Academic Profile

Statistics

Similar Authors

Papers on arXiv

In the present paper, we derive a closed-form solution of the multi-period portfolio choice problem for a quadratic utility function with and without a riskless asset. All results are derived under ...

In this paper we derive the exact solution of the multi-period portfolio choice problem for an exponential utility function under return predictability. It is assumed that the asset returns depend o...

In this work we construct an optimal shrinkage estimator for the precision matrix in high dimensions. We consider the general asymptotics when the number of variables $p\rightarrow\infty$ and the sa...

We estimate the global minimum variance (GMV) portfolio in the high-dimensional case using results from random matrix theory. This approach leads to a shrinkage-type estimator which is distribution-...

In this paper we consider the asymptotic distributions of functionals of the sample covariance matrix and the sample mean vector obtained under the assumption that the matrix of observations has a m...

In this paper we estimate the mean-variance portfolio in the high-dimensional case using the recent results from the theory of random matrices. We construct a linear shrinkage estimator which is dis...

In this paper, we derive high-dimensional asymptotic properties of the Moore-Penrose inverse and the ridge-type inverse of the sample covariance matrix. In particular, the analytical expressions of ...

In this paper, we present the Bayesian inference procedures for the parameters of the multivariate random effects model derived under the assumption of an elliptically contoured distribution when th...

The sub-Gaussian stable distribution is a heavy-tailed elliptically contoured law which has interesting applications in signal processing and financial mathematics. This work addresses the problem o...

In this paper, a new way to integrate volatility information for estimating value at risk (VaR) and conditional value at risk (CVaR) of a portfolio is suggested. The new method is developed from the...

In this paper we construct a shrinkage estimator of the global minimum variance (GMV) portfolio by a combination of two techniques: Tikhonov regularization and direct shrinkage of portfolio weights....

The main contribution of this paper is the derivation of the asymptotic behaviour of the out-of-sample variance, the out-of-sample relative loss, and of their empirical counterparts in the high-dime...

In this paper, new results in random matrix theory are derived which allow us to construct a shrinkage estimator of the global minimum variance (GMV) portfolio when the shrinkage target is a random ...

Objective Bayesian inference procedures are derived for the parameters of the multivariate random effects model generalized to elliptically contoured distributions. The posterior for the overall mea...

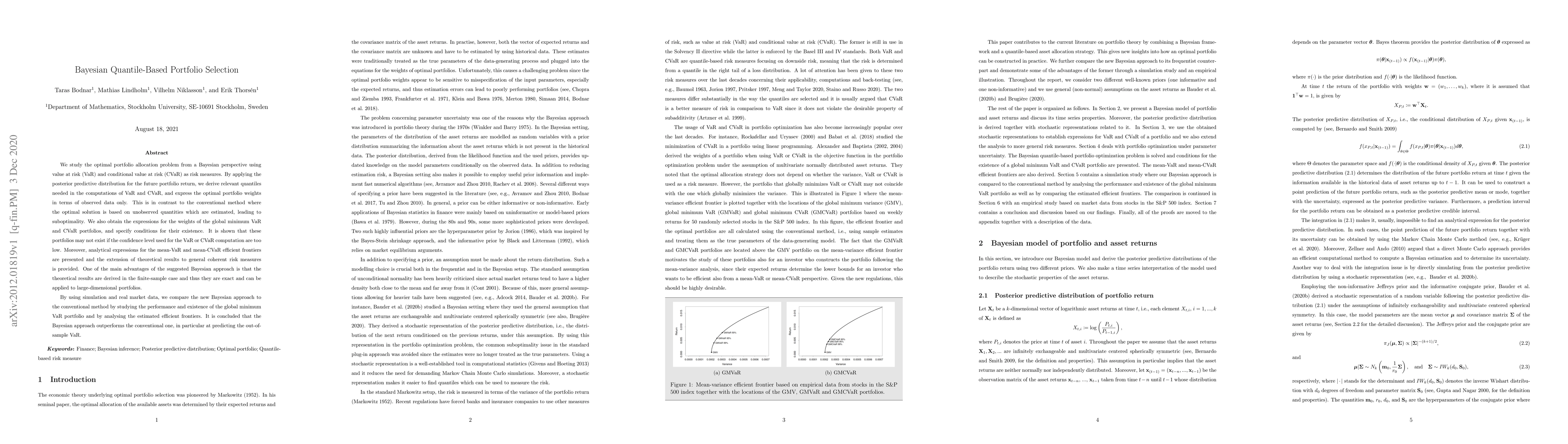

We study the optimal portfolio allocation problem from a Bayesian perspective using value at risk (VaR) and conditional value at risk (CVaR) as risk measures. By applying the posterior predictive di...

In this paper, using the shrinkage-based approach for portfolio weights and modern results from random matrix theory we construct an effective procedure for testing the efficiency of the expected ut...

A reflexive generalized inverse and the Moore-Penrose inverse are often confused in statistical literature but in fact they have completely different behaviour in case the population covariance matr...

Optimal portfolio selection problems are determined by the (unknown) parameters of the data generating process. If an investor wants to realise the position suggested by the optimal portfolios, he/s...

We derive new results related to the portfolio choice problem for power and logarithmic utilities. Assuming that the portfolio returns follow an approximate log-normal distribution, the closed-form ...

The paper solves the problem of optimal portfolio choice when the parameters of the asset returns distribution, like the mean vector and the covariance matrix are unknown and have to be estimated by...

In this study, we construct two tests for the weights of the global minimum variance portfolio (GMVP) in a high-dimensional setting, namely, when the number of assets $p$ depends on the sample size ...

In this paper new tests for the independence of two high-dimensional vectors are investigated. We consider the case where the dimension of the vectors increases with the sample size and propose mult...

We consider the estimation of the multi-period optimal portfolio obtained by maximizing an exponential utility. Employing Jeffreys' non-informative prior and the conjugate informative prior, we deri...

In this paper, we analyze the asymptotic behavior of the main characteristics of the mean-variance efficient frontier employing random matrix theory. Our particular interest covers the case when the d...