Academic Profile

Statistics

Similar Authors

Papers on arXiv

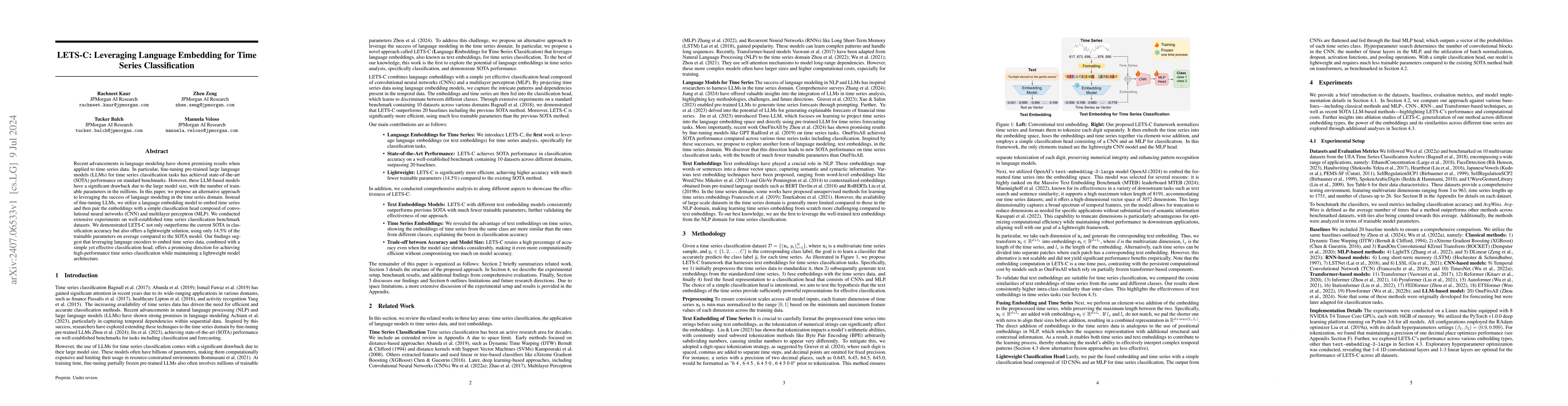

Recent advancements in language modeling have shown promising results when applied to time series data. In particular, fine-tuning pre-trained large language models (LLMs) for time series classificati...

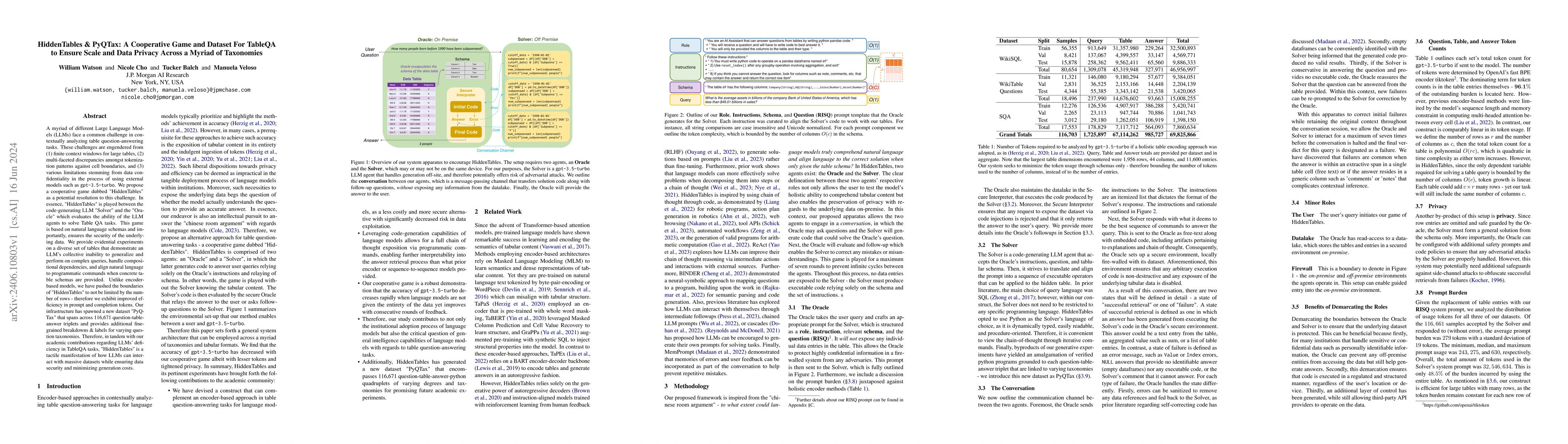

A myriad of different Large Language Models (LLMs) face a common challenge in contextually analyzing table question-answering tasks. These challenges are engendered from (1) finite context windows f...

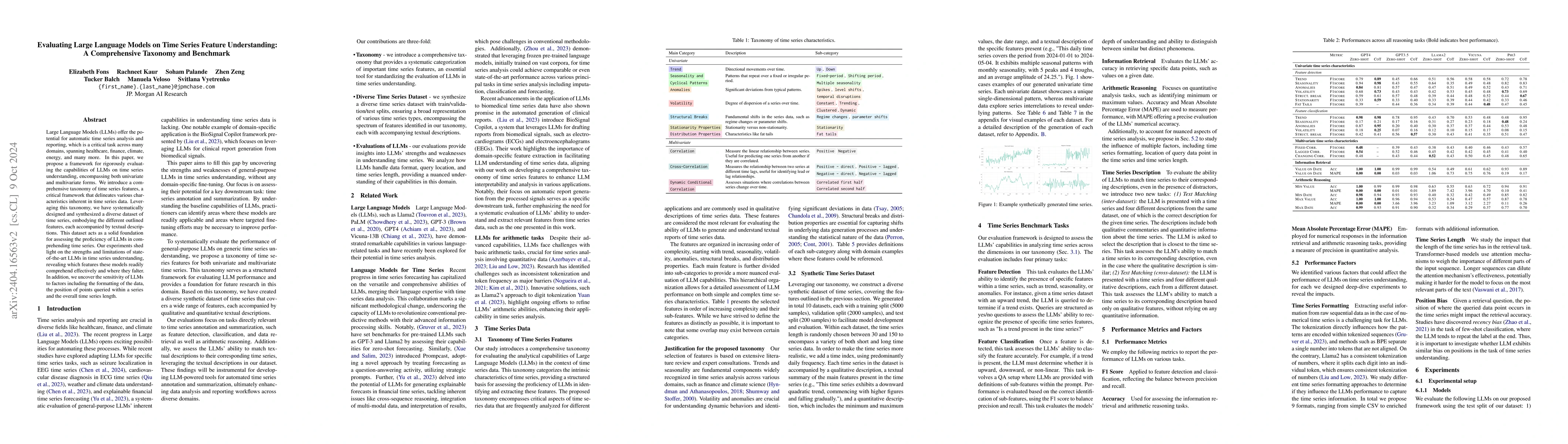

Large Language Models (LLMs) offer the potential for automatic time series analysis and reporting, which is a critical task across many domains, spanning healthcare, finance, climate, energy, and ma...

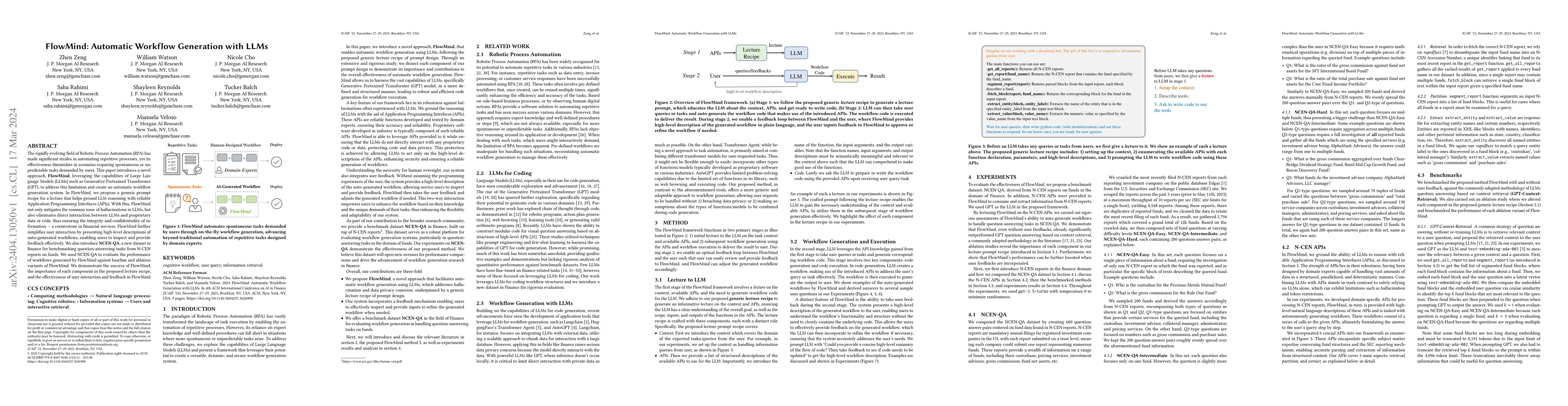

The rapidly evolving field of Robotic Process Automation (RPA) has made significant strides in automating repetitive processes, yet its effectiveness diminishes in scenarios requiring spontaneous or...

Banks publish daily a list of available securities/assets (axe list) to selected clients to help them effectively locate Long (buy) or Short (sell) trades at reduced financing rates. This reduces co...

Synthetic Data is increasingly important in financial applications. In addition to the benefits it provides, such as improved financial modeling and better testing procedures, it poses privacy risks...

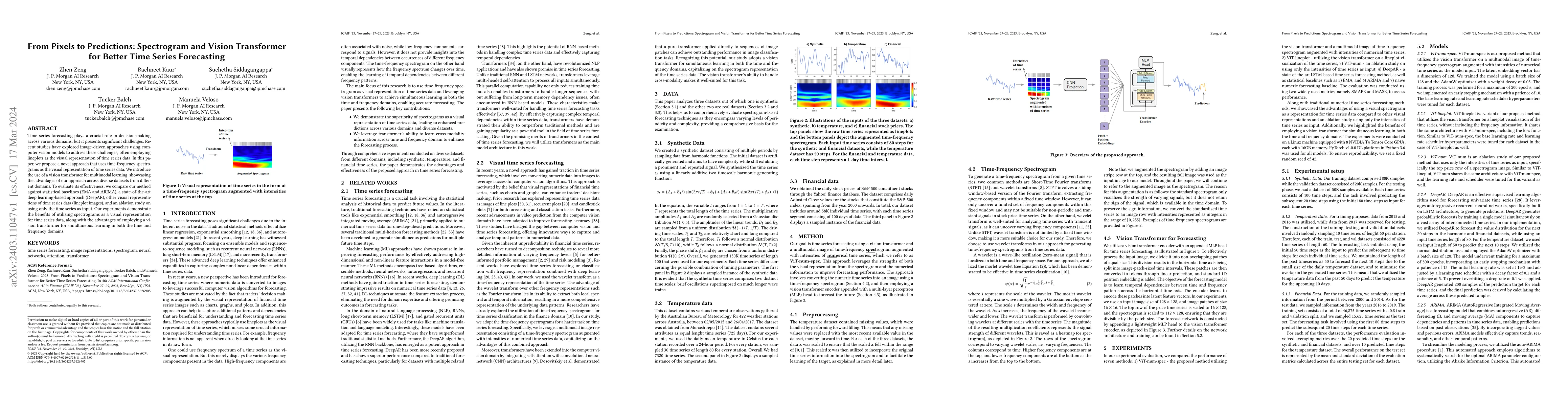

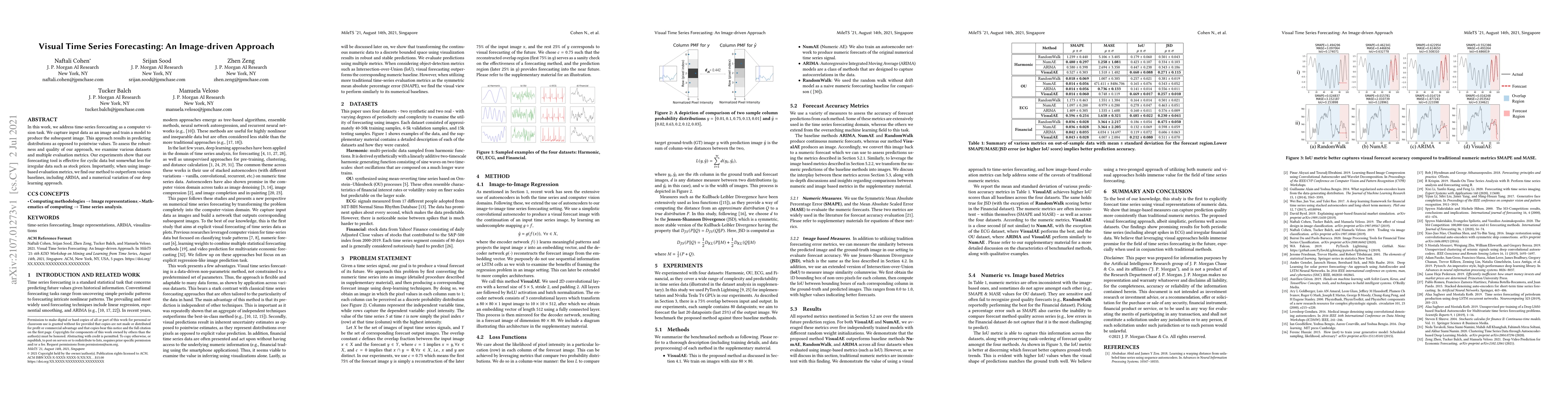

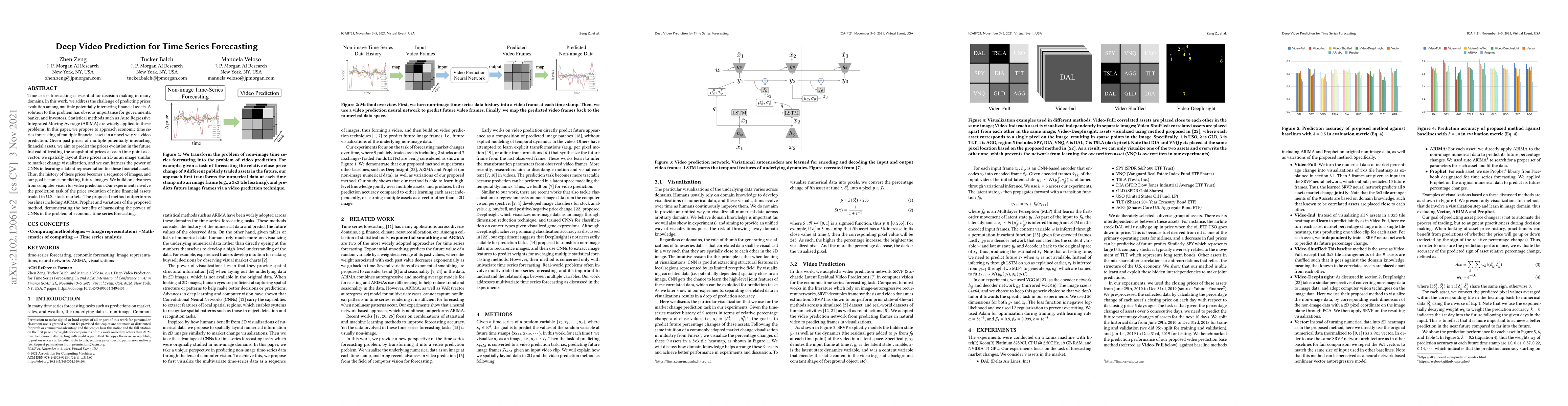

Time series forecasting plays a crucial role in decision-making across various domains, but it presents significant challenges. Recent studies have explored image-driven approaches using computer vi...

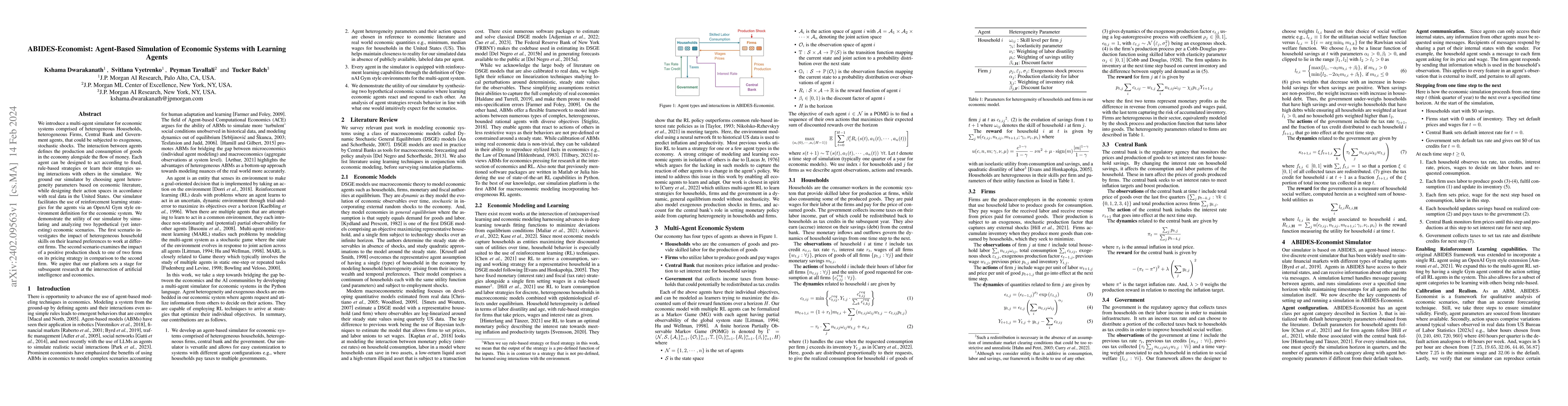

We introduce a multi-agent simulator for economic systems comprised of heterogeneous Households, heterogeneous Firms, Central Bank and Government agents, that could be subjected to exogenous, stocha...

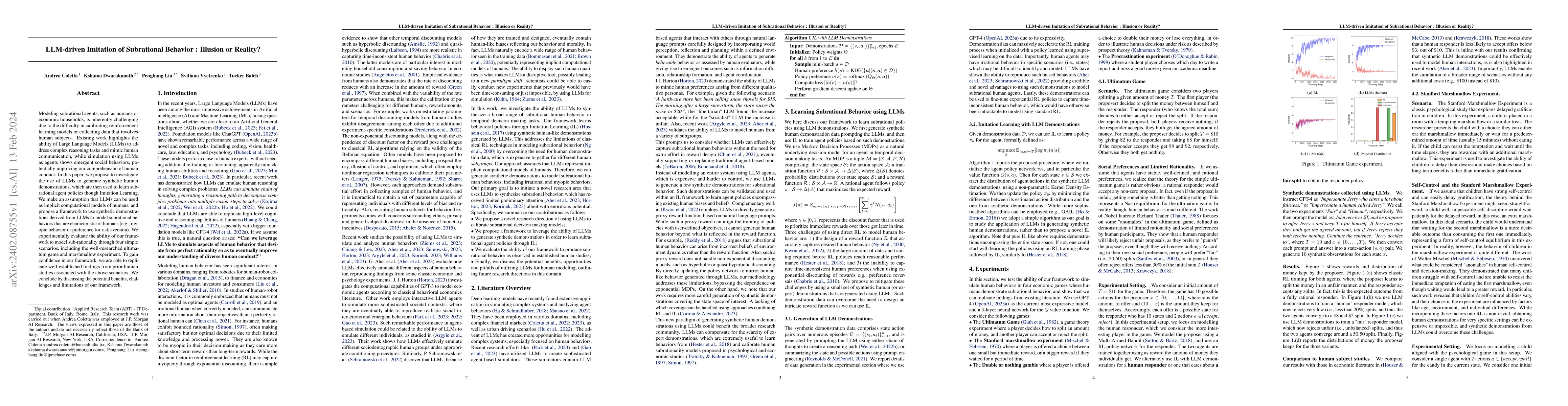

Modeling subrational agents, such as humans or economic households, is inherently challenging due to the difficulty in calibrating reinforcement learning models or collecting data that involves huma...

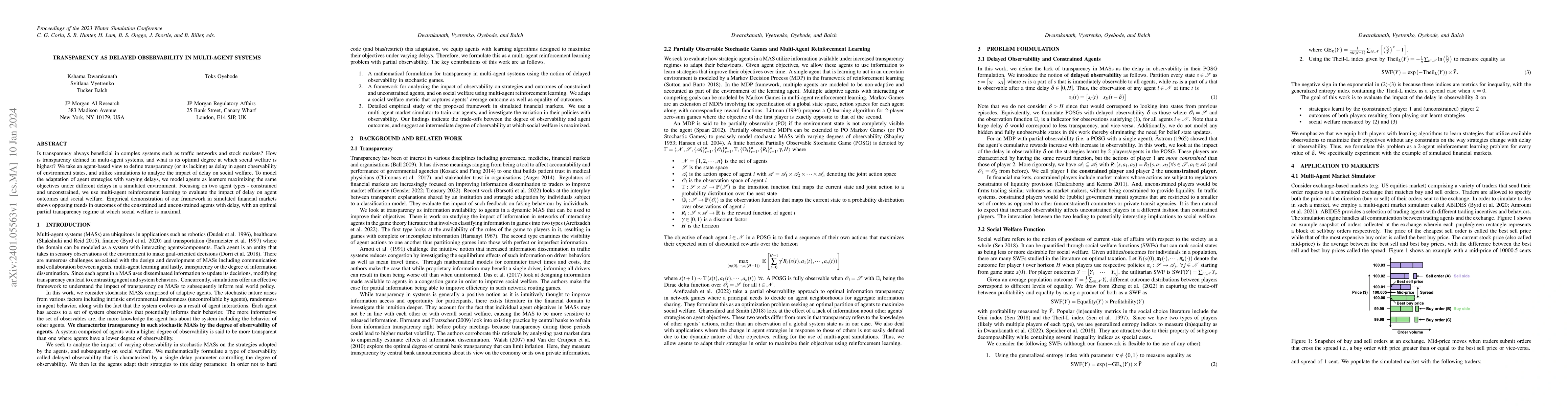

Is transparency always beneficial in complex systems such as traffic networks and stock markets? How is transparency defined in multi-agent systems, and what is its optimal degree at which social we...

Devising procedures for downstream task-oriented generative model selections is an unresolved problem of practical importance. Existing studies focused on the utility of a single family of generativ...

Synthetic data has made tremendous strides in various commercial settings including finance, healthcare, and virtual reality. We present a broad overview of prototypical applications of synthetic da...

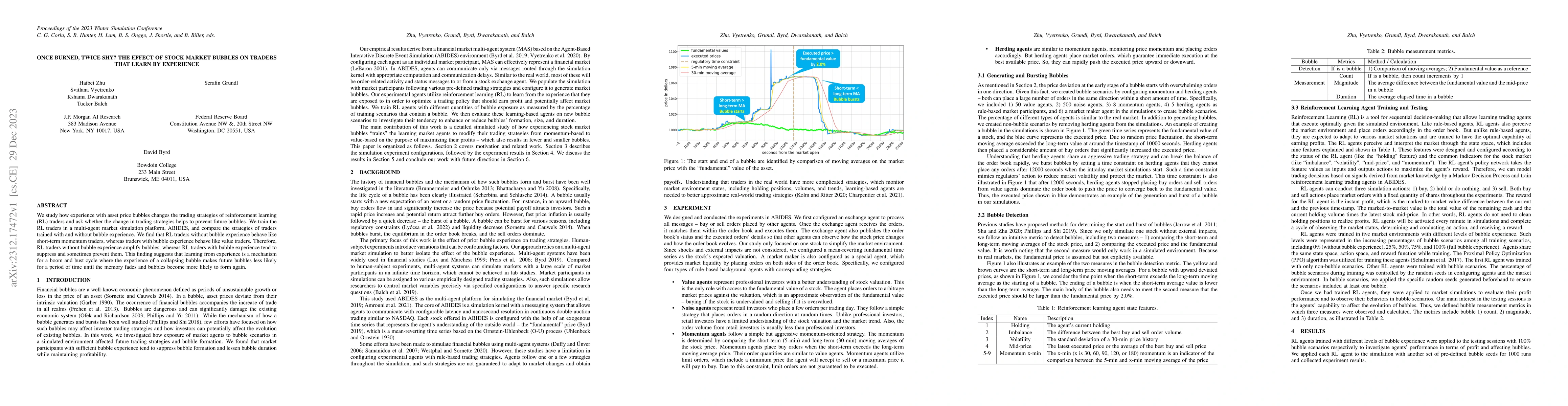

We study how experience with asset price bubbles changes the trading strategies of reinforcement learning (RL) traders and ask whether the change in trading strategies helps to prevent future bubble...

Data distillation and coresets have emerged as popular approaches to generate a smaller representative set of samples for downstream learning tasks to handle large-scale datasets. At the same time, ...

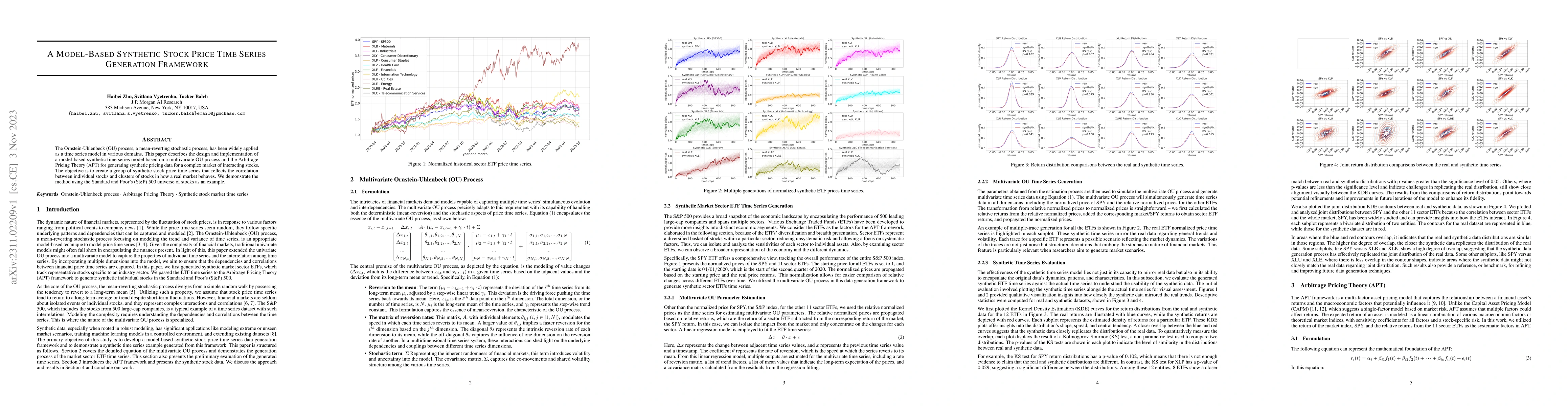

The Ornstein-Uhlenbeck (OU) process, a mean-reverting stochastic process, has been widely applied as a time series model in various domains. This paper describes the design and implementation of a m...

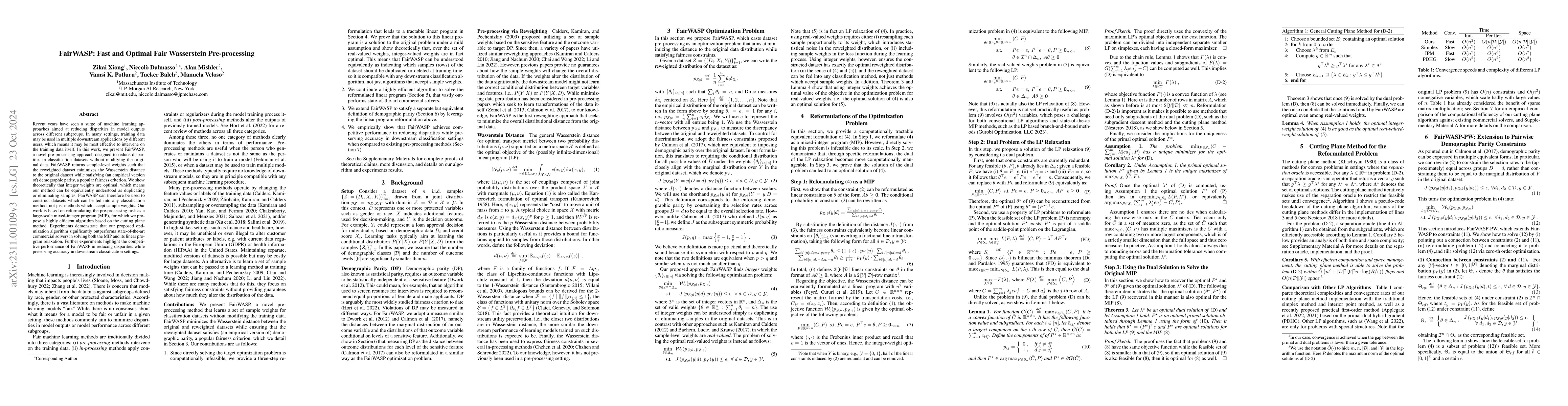

Recent years have seen a surge of machine learning approaches aimed at reducing disparities in model outputs across different subgroups. In many settings, training data may be used in multiple downs...

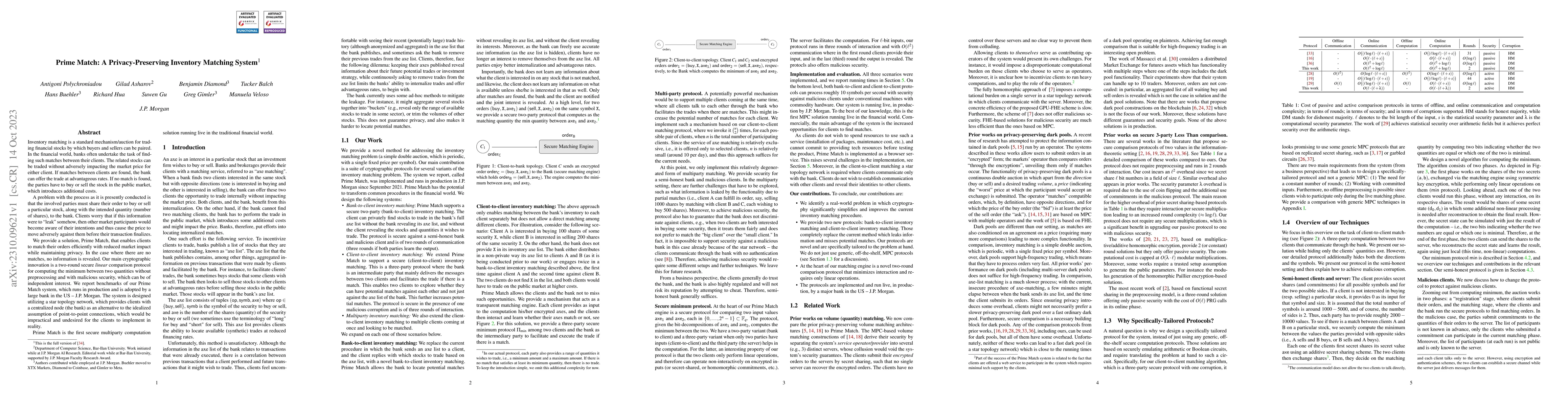

Inventory matching is a standard mechanism/auction for trading financial stocks by which buyers and sellers can be paired. In the financial world, banks often undertake the task of finding such matc...

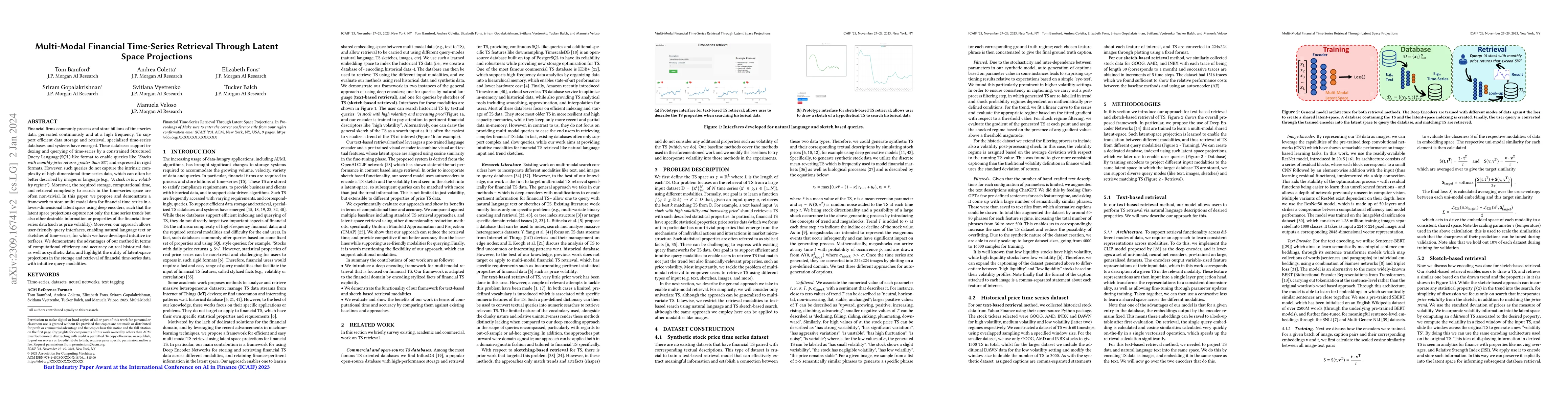

Financial firms commonly process and store billions of time-series data, generated continuously and at a high frequency. To support efficient data storage and retrieval, specialized time-series data...

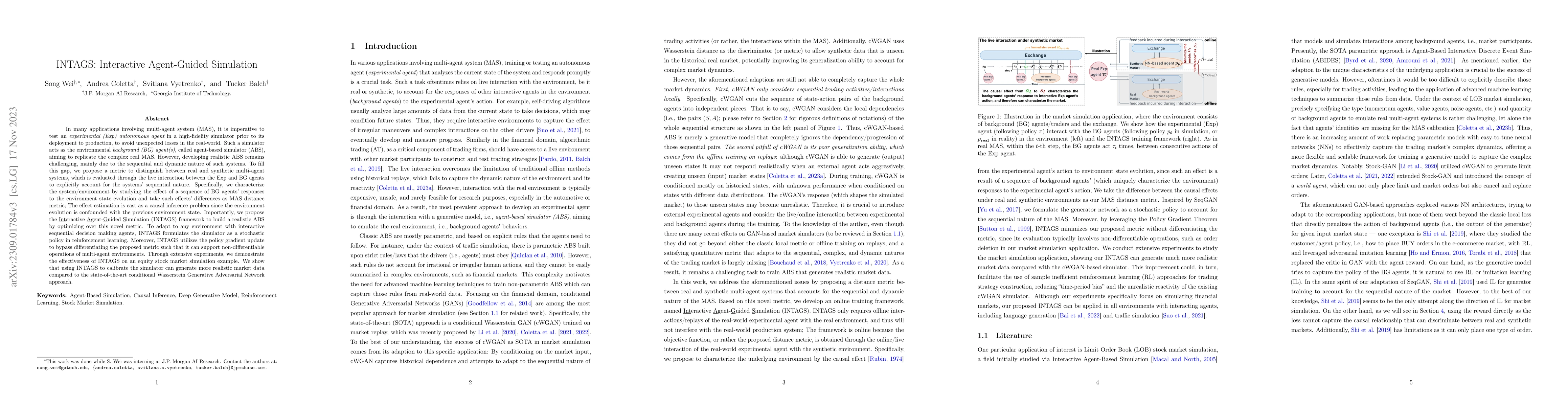

In many applications involving multi-agent system (MAS), it is imperative to test an experimental (Exp) autonomous agent in a high-fidelity simulator prior to its deployment to production, to avoid ...

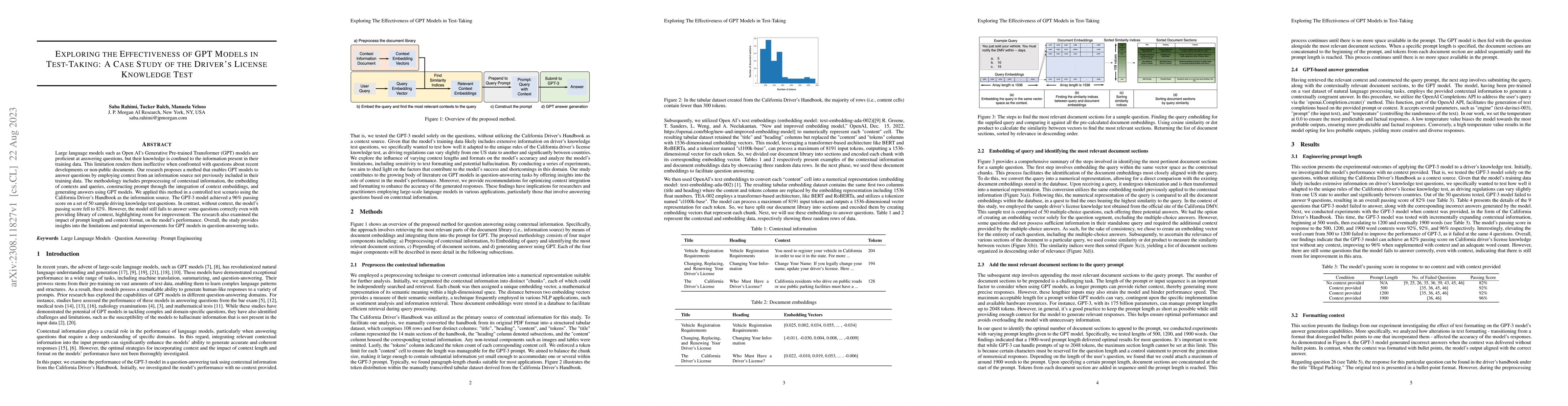

Large language models such as Open AI's Generative Pre-trained Transformer (GPT) models are proficient at answering questions, but their knowledge is confined to the information present in their tra...

Creation of a synthetic dataset that faithfully represents the data distribution and simultaneously preserves privacy is a major research challenge. Many space partitioning based approaches have eme...

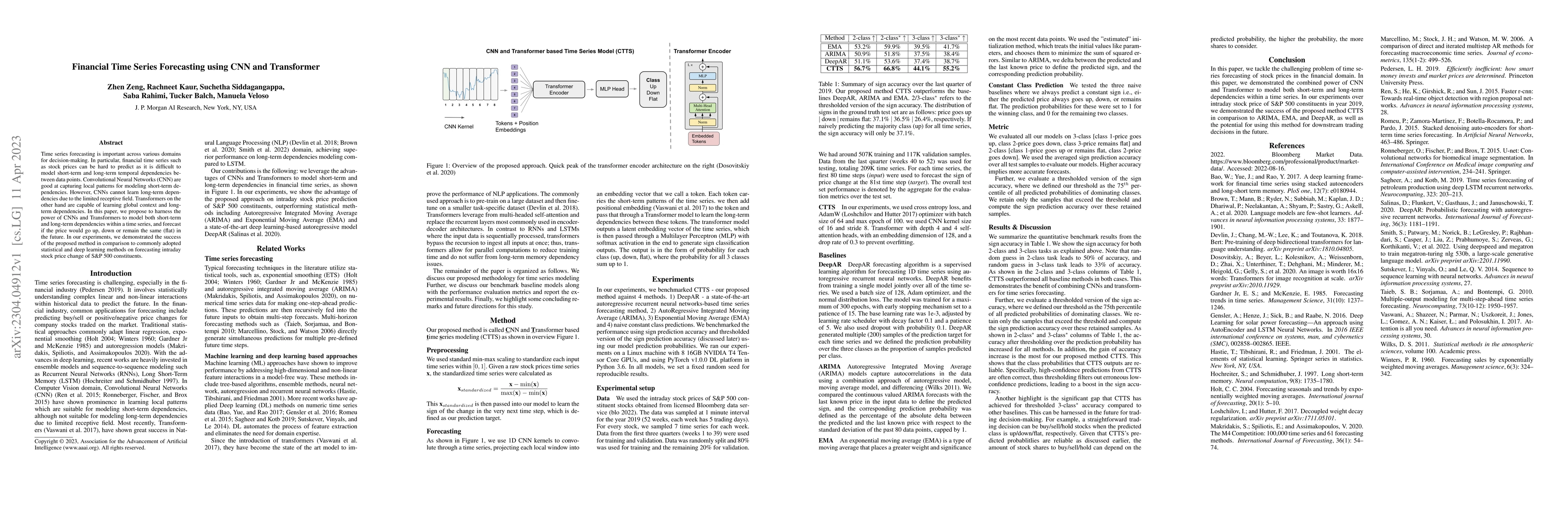

Time series forecasting is important across various domains for decision-making. In particular, financial time series such as stock prices can be hard to predict as it is difficult to model short-te...

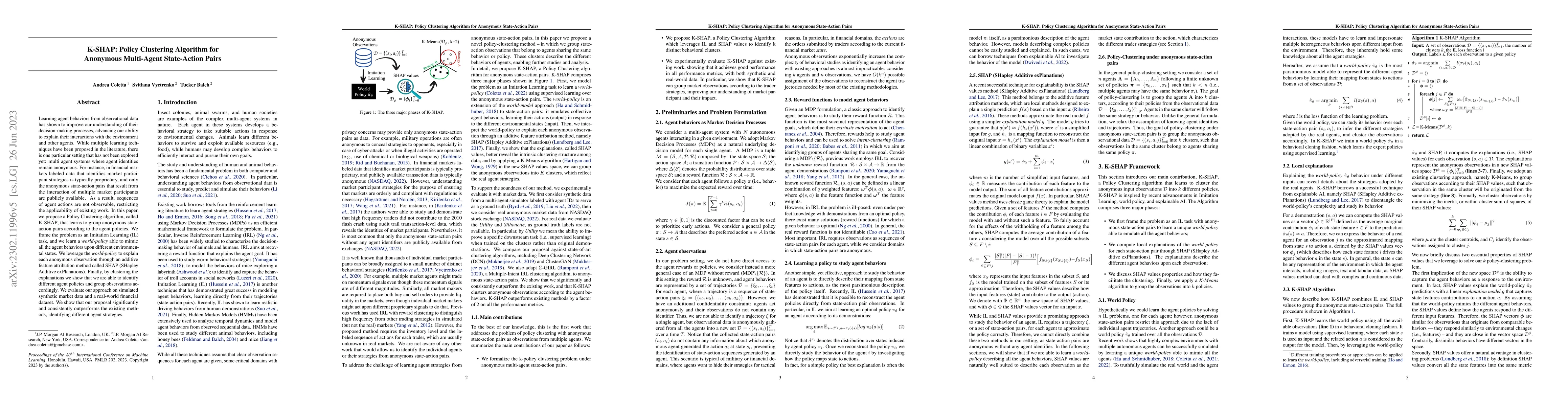

Learning agent behaviors from observational data has shown to improve our understanding of their decision-making processes, advancing our ability to explain their interactions with the environment a...

Hawkes processes have recently risen to the forefront of tools when it comes to modeling and generating sequential events data. Multidimensional Hawkes processes model both the self and cross-excita...

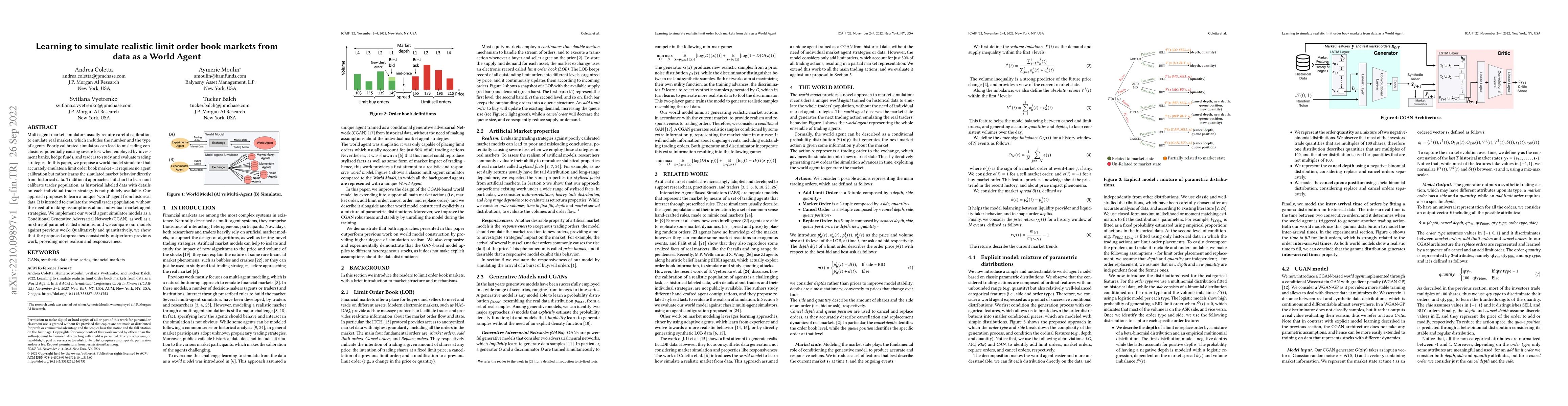

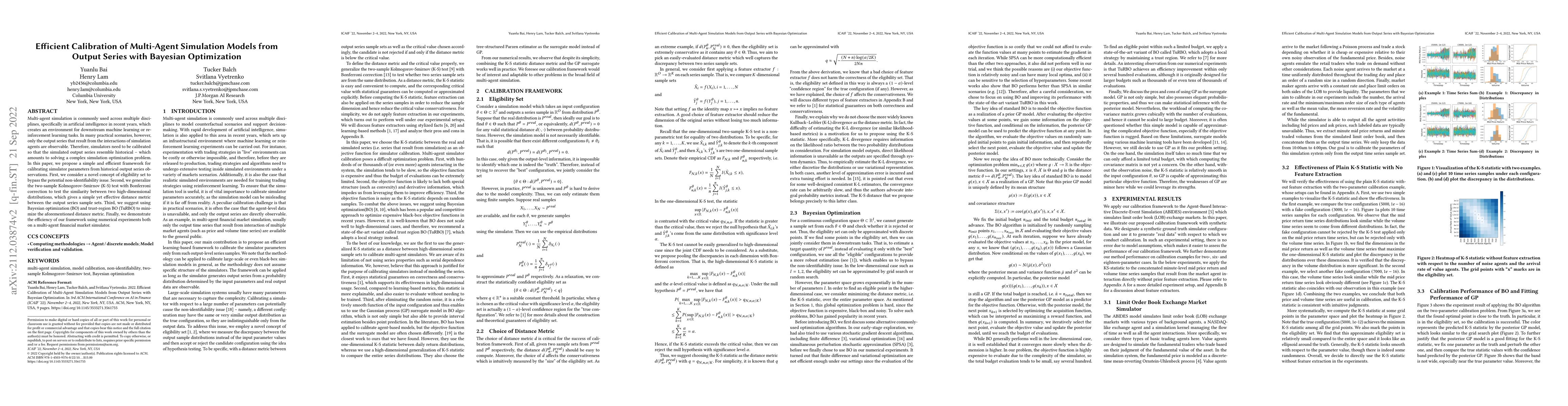

Multi-agent market simulators usually require careful calibration to emulate real markets, which includes the number and the type of agents. Poorly calibrated simulators can lead to misleading concl...

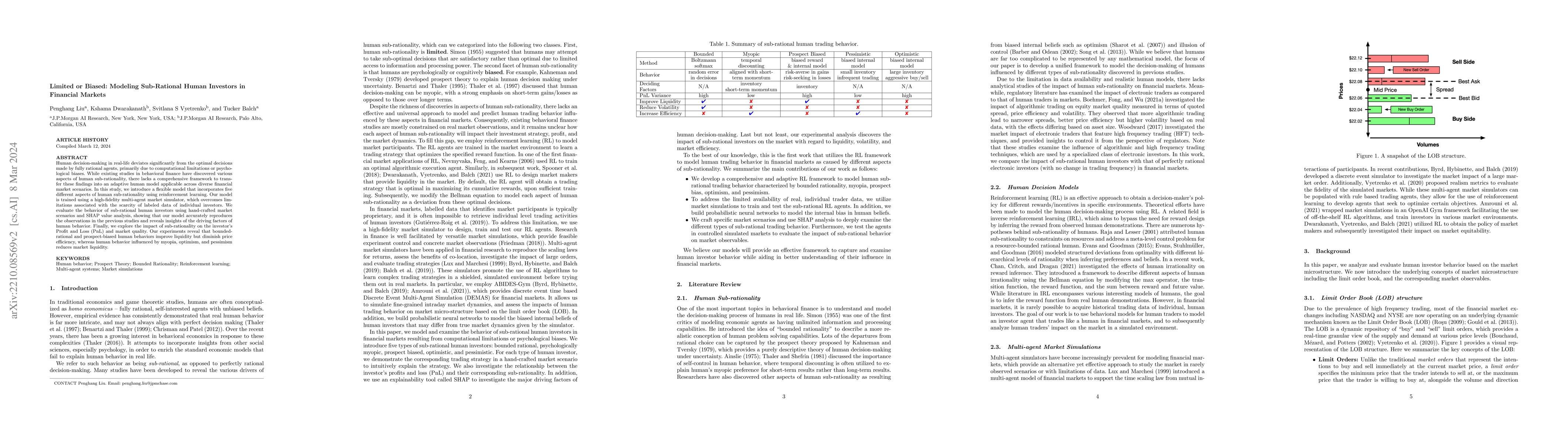

Human decision-making in real-life deviates significantly from the optimal decisions made by fully rational agents, primarily due to computational limitations or psychological biases. While existing...

We study a game between liquidity provider and liquidity taker agents interacting in an over-the-counter market, for which the typical example is foreign exchange. We show how a suitable design of p...

We consider a trading marketplace that is populated by traders with diverse trading strategies and objectives. The marketplace allows the suppliers to list their goods and facilitates matching betwe...

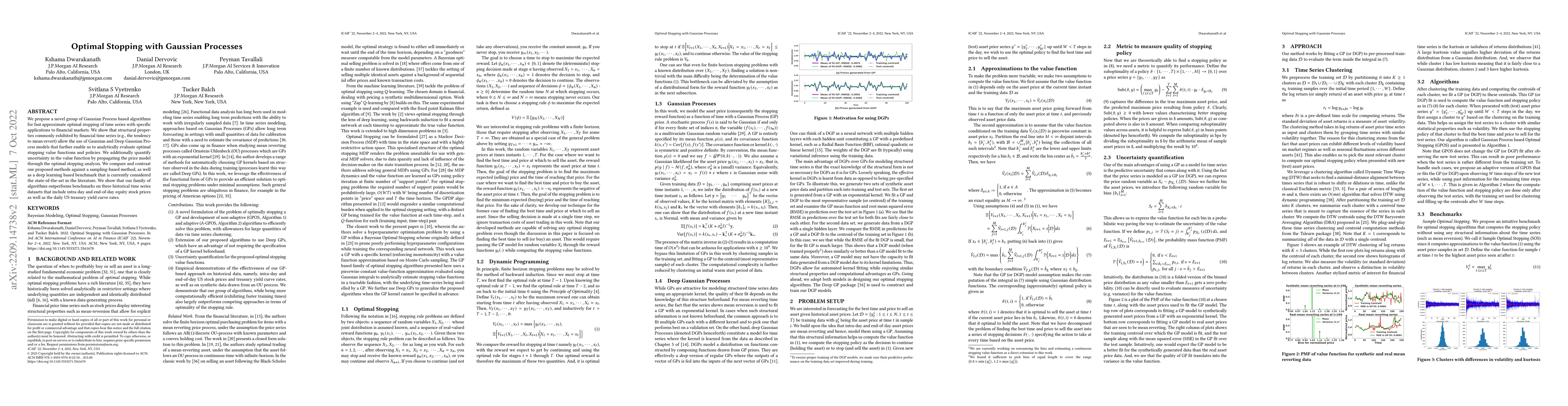

We propose a novel group of Gaussian Process based algorithms for fast approximate optimal stopping of time series with specific applications to financial markets. We show that structural properties...

Online learning of Hawkes processes has received increasing attention in the last couple of years especially for modeling a network of actors. However, these works typically either model the rich in...

Hawkes processes have recently gained increasing attention from the machine learning community for their versatility in modeling event sequence data. While they have a rich history going back decade...

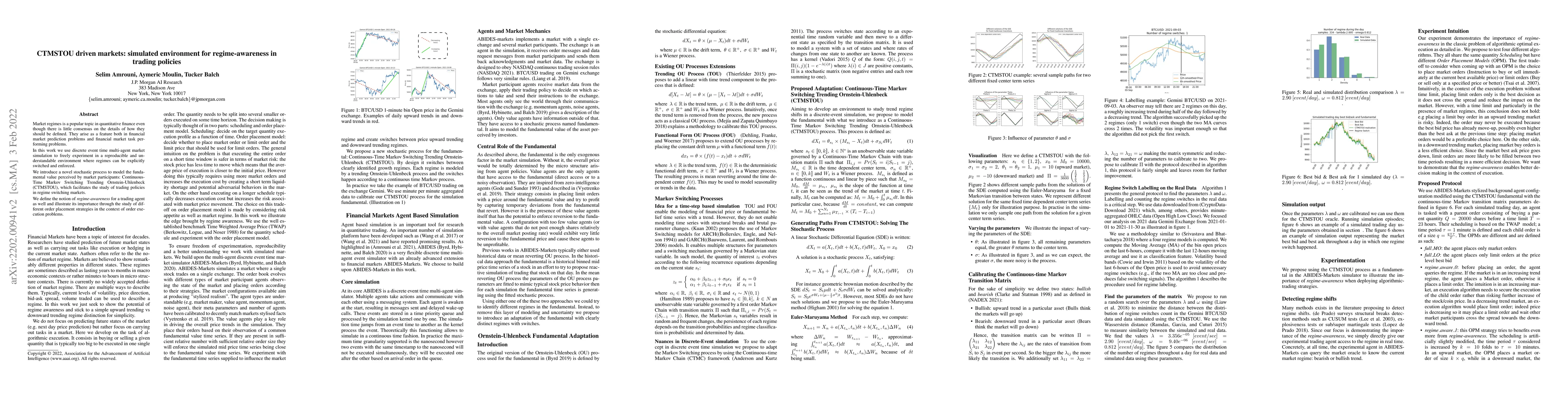

Market regimes is a popular topic in quantitative finance even though there is little consensus on the details of how they should be defined. They arise as a feature both in financial market predict...

Multi-agent simulation is commonly used across multiple disciplines, specifically in artificial intelligence in recent years, which creates an environment for downstream machine learning or reinforc...

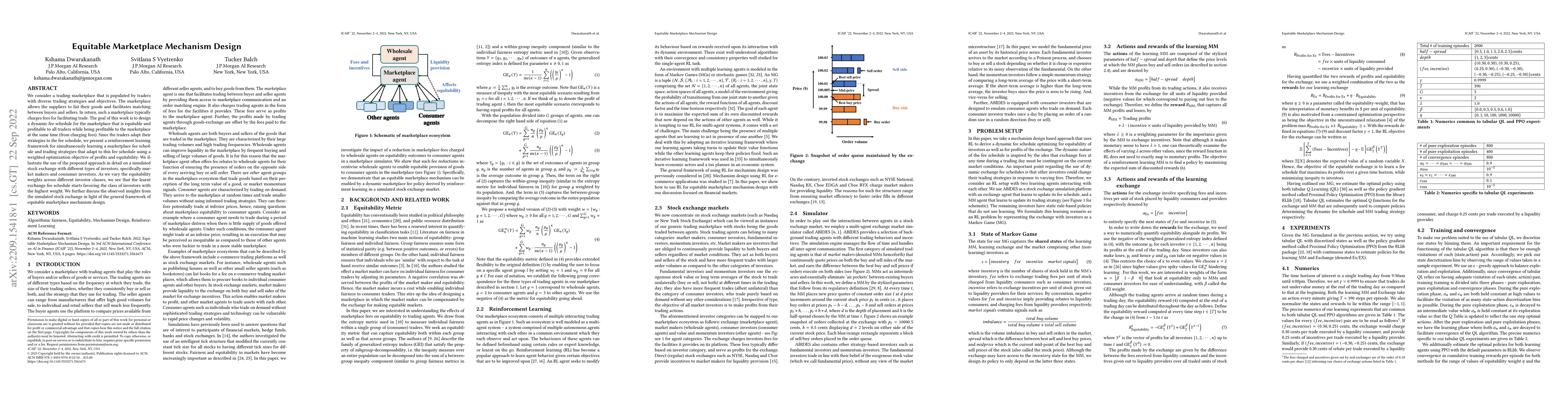

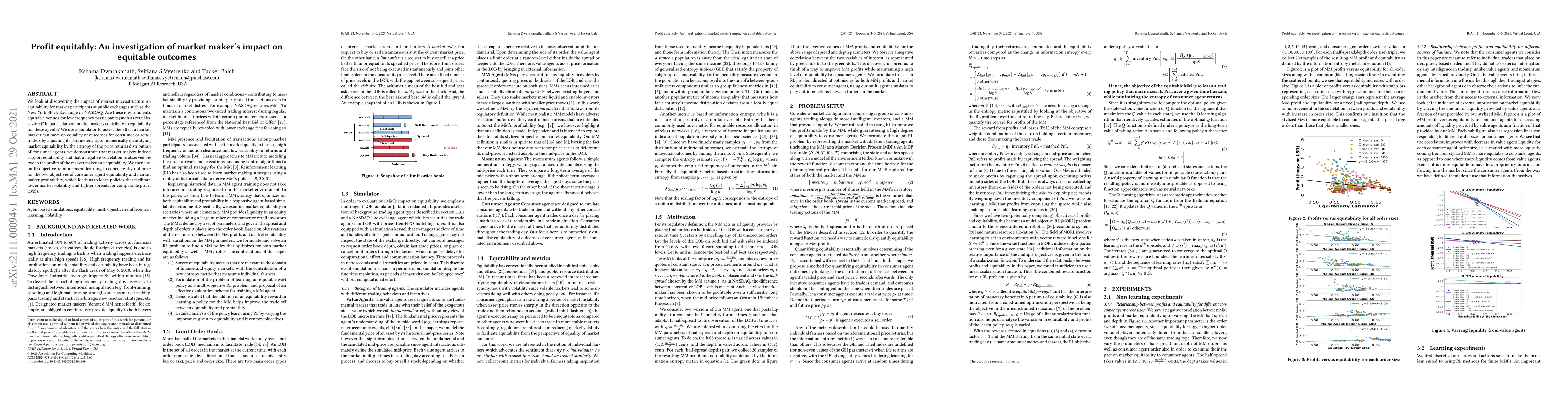

We look at discovering the impact of market microstructure on equitability for market participants at public exchanges such as the New York Stock Exchange or NASDAQ. Are these environments equitable...

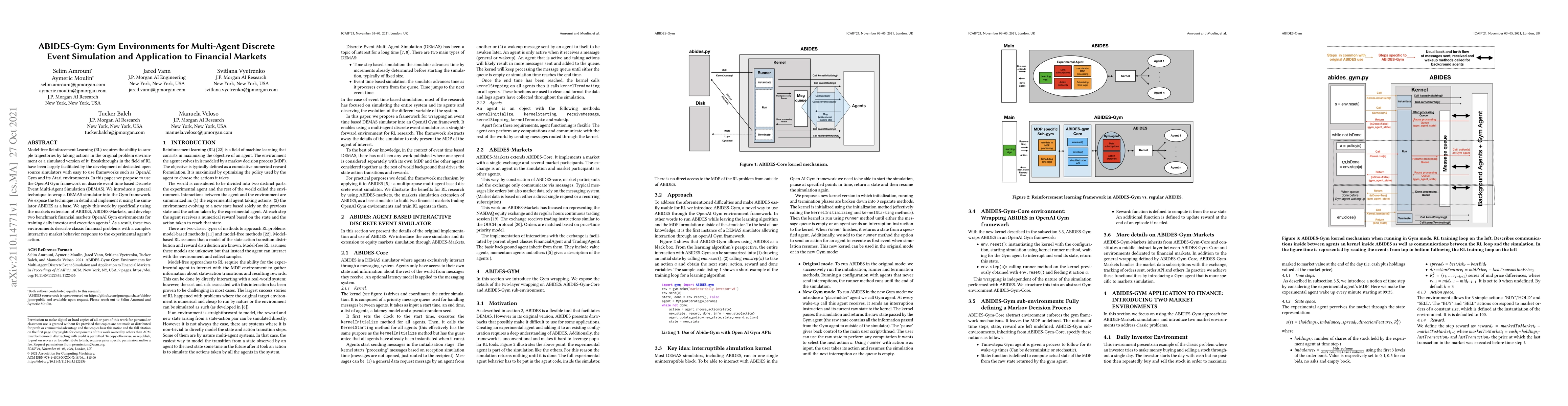

Model-free Reinforcement Learning (RL) requires the ability to sample trajectories by taking actions in the original problem environment or a simulated version of it. Breakthroughs in the field of R...

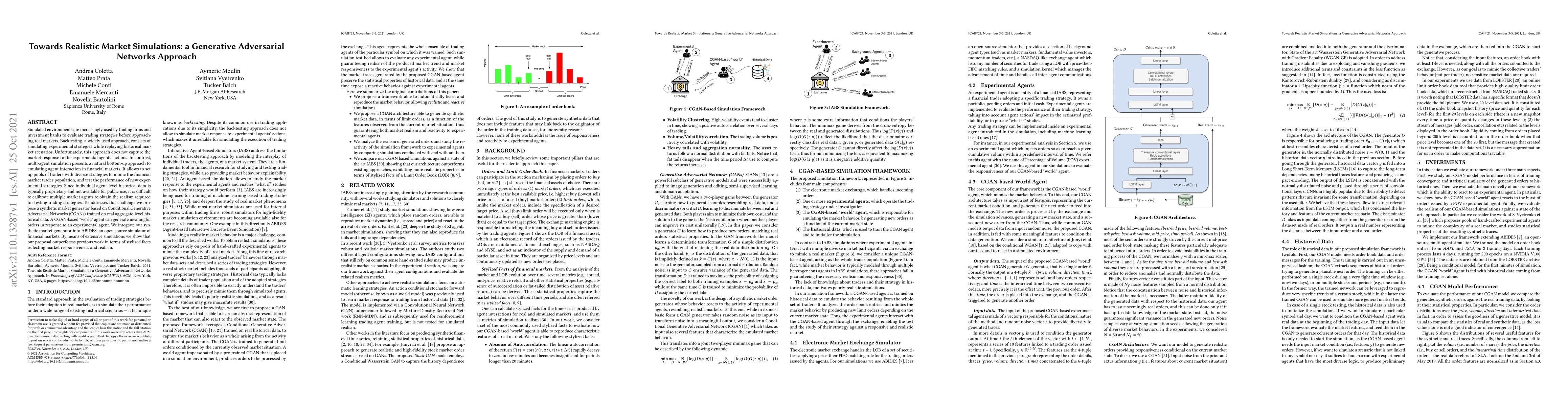

Simulated environments are increasingly used by trading firms and investment banks to evaluate trading strategies before approaching real markets. Backtesting, a widely used approach, consists of si...

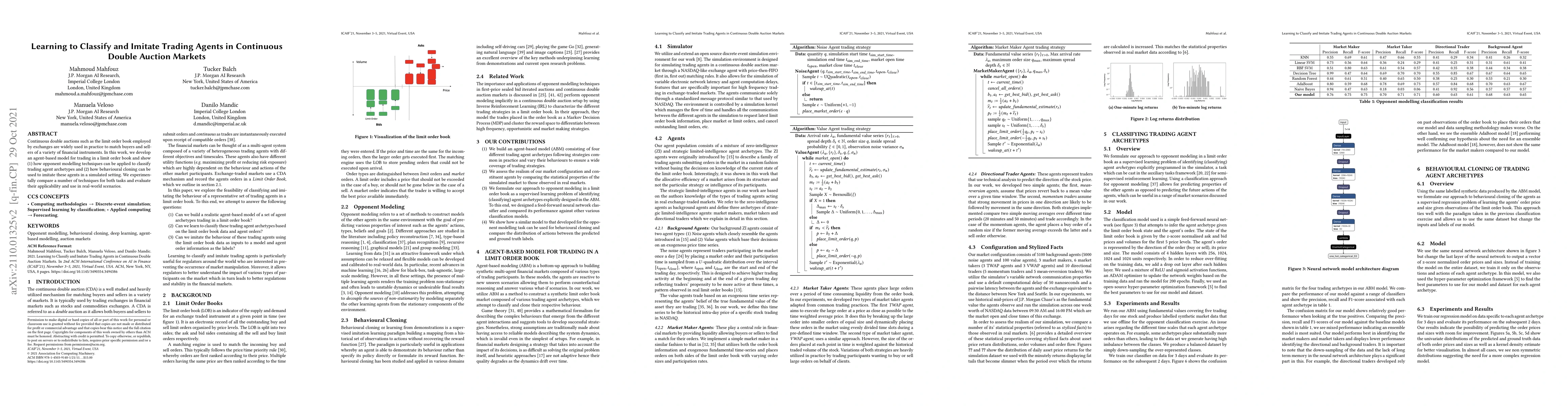

Continuous double auctions such as the limit order book employed by exchanges are widely used in practice to match buyers and sellers of a variety of financial instruments. In this work, we develop ...

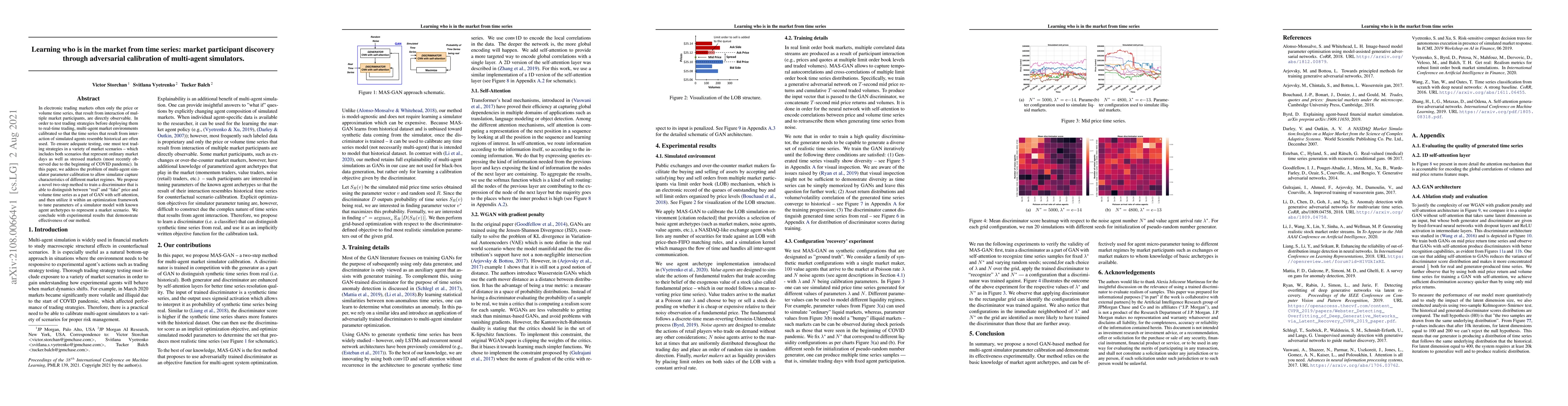

In electronic trading markets often only the price or volume time series, that result from interaction of multiple market participants, are directly observable. In order to test trading strategies b...

In this work, we address time-series forecasting as a computer vision task. We capture input data as an image and train a model to produce the subsequent image. This approach results in predicting d...

Stochastic simulation aims to compute output performance for complex models that lack analytical tractability. To ensure accurate prediction, the model needs to be calibrated and validated against r...

Time series forecasting is essential for decision making in many domains. In this work, we address the challenge of predicting prices evolution among multiple potentially interacting financial asset...

Supervised learning classifiers inevitably make mistakes in production, perhaps mis-labeling an email, or flagging an otherwise routine transaction as fraudulent. It is vital that the end users of s...

Document classification is ubiquitous in a business setting, but often the end users of a classifier are engaged in an ongoing feedback-retrain loop with the team that maintain it. We consider this ...

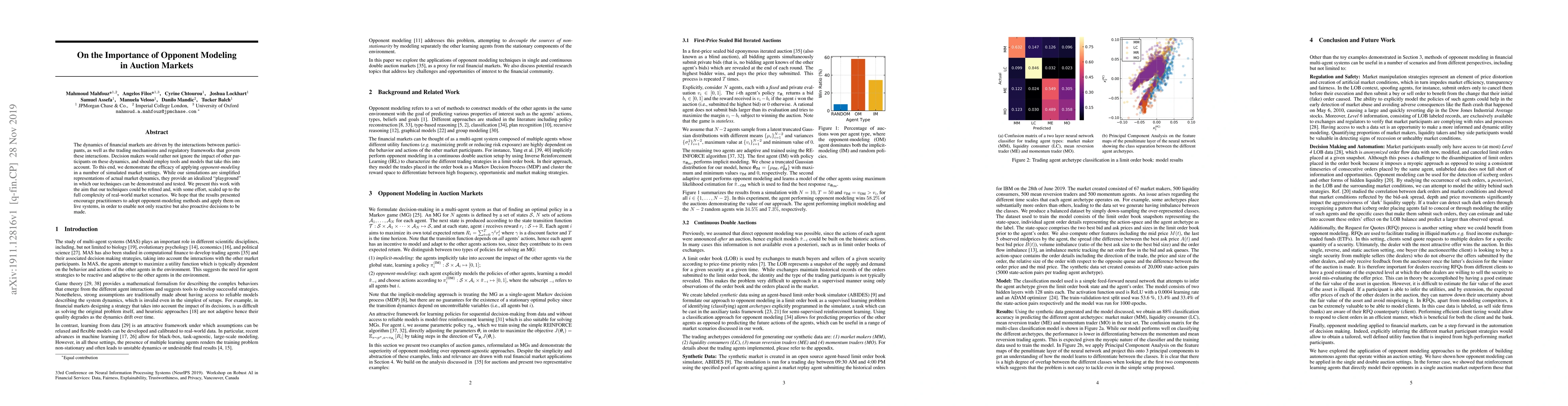

The dynamics of financial markets are driven by the interactions between participants, as well as the trading mechanisms and regulatory frameworks that govern these interactions. Decision-makers wou...

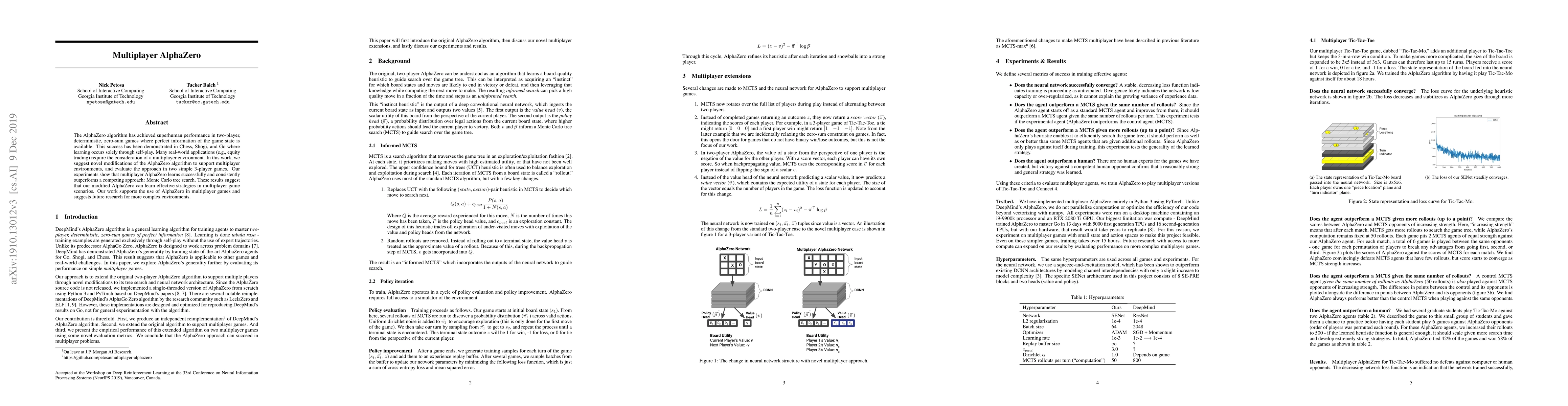

The AlphaZero algorithm has achieved superhuman performance in two-player, deterministic, zero-sum games where perfect information of the game state is available. This success has been demonstrated ...

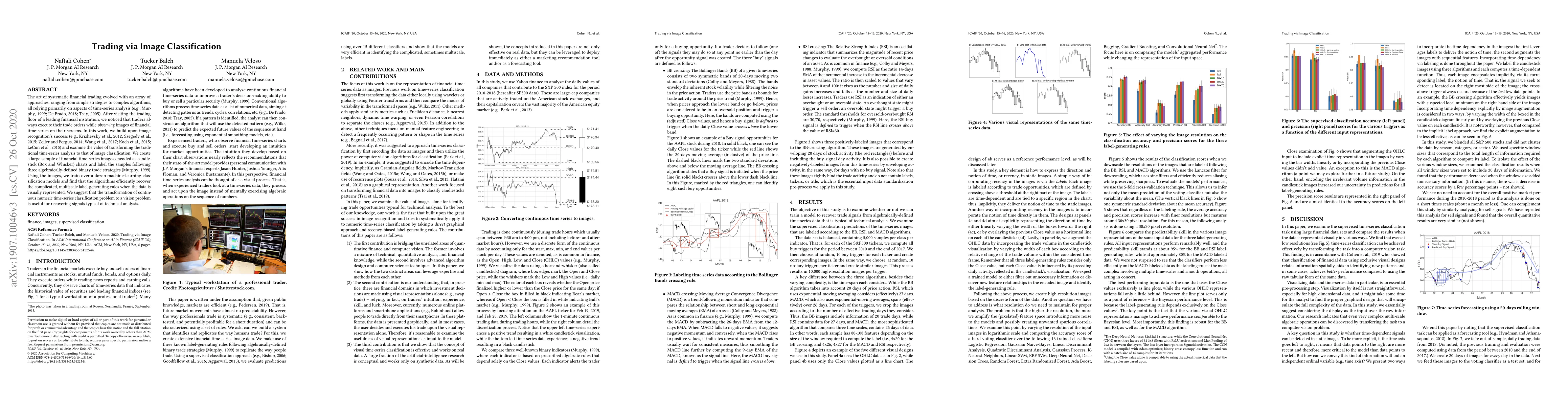

The art of systematic financial trading evolved with an array of approaches, ranging from simple strategies to complex algorithms all relying, primary, on aspects of time-series analysis. Recently, ...

Financial companies continuously analyze the state of the markets to rethink and adjust their investment strategies. While the analysis is done on the digital form of data, decisions are often made ...

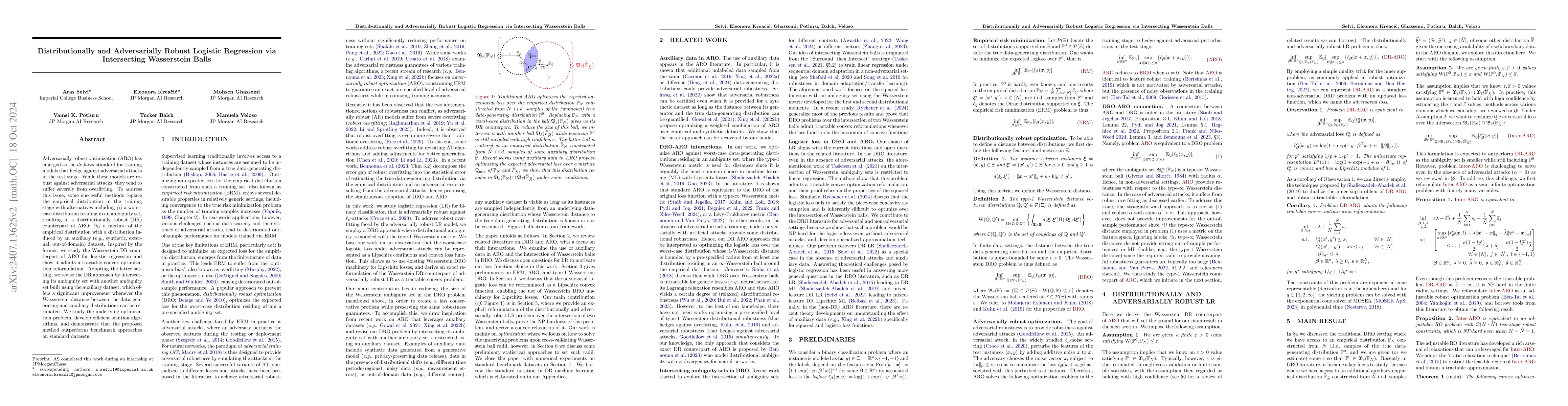

Empirical risk minimization often fails to provide robustness against adversarial attacks in test data, causing poor out-of-sample performance. Adversarially robust optimization (ARO) has thus emerged...

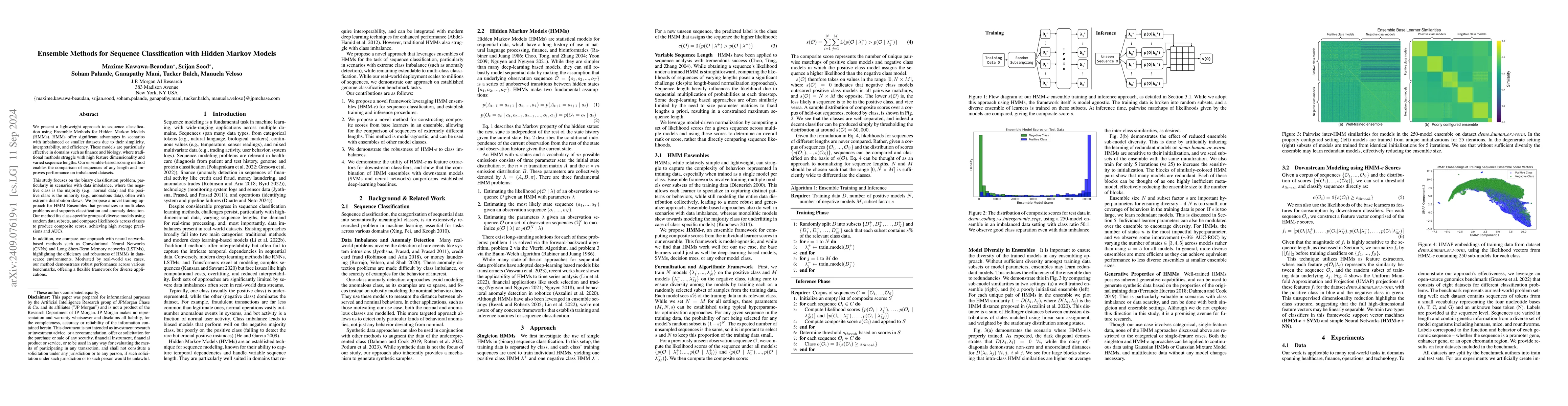

We present a lightweight approach to sequence classification using Ensemble Methods for Hidden Markov Models (HMMs). HMMs offer significant advantages in scenarios with imbalanced or smaller datasets ...

Adoption of AI by criminal entities across traditional and emerging financial crime paradigms has been a disturbing recent trend. Particularly concerning is the proliferation of generative AI, which h...

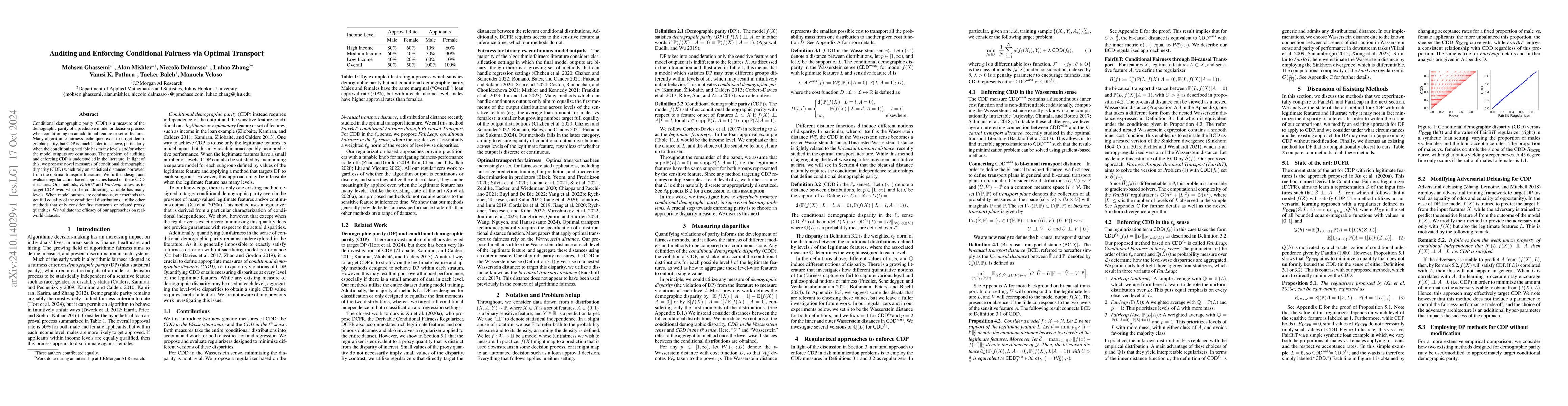

Conditional demographic parity (CDP) is a measure of the demographic parity of a predictive model or decision process when conditioning on an additional feature or set of features. Many algorithmic fa...

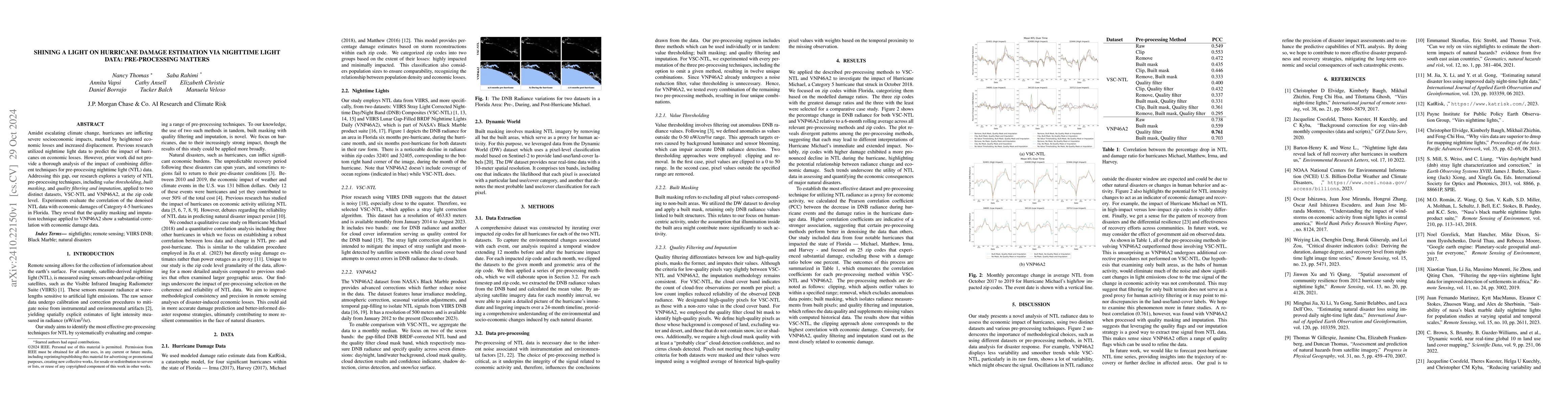

Amidst escalating climate change, hurricanes are inflicting severe socioeconomic impacts, marked by heightened economic losses and increased displacement. Previous research utilized nighttime light da...

We investigate the use of sequence analysis for behavior modeling, emphasizing that sequential context often outweighs the value of aggregate features in understanding human behavior. We discuss frami...

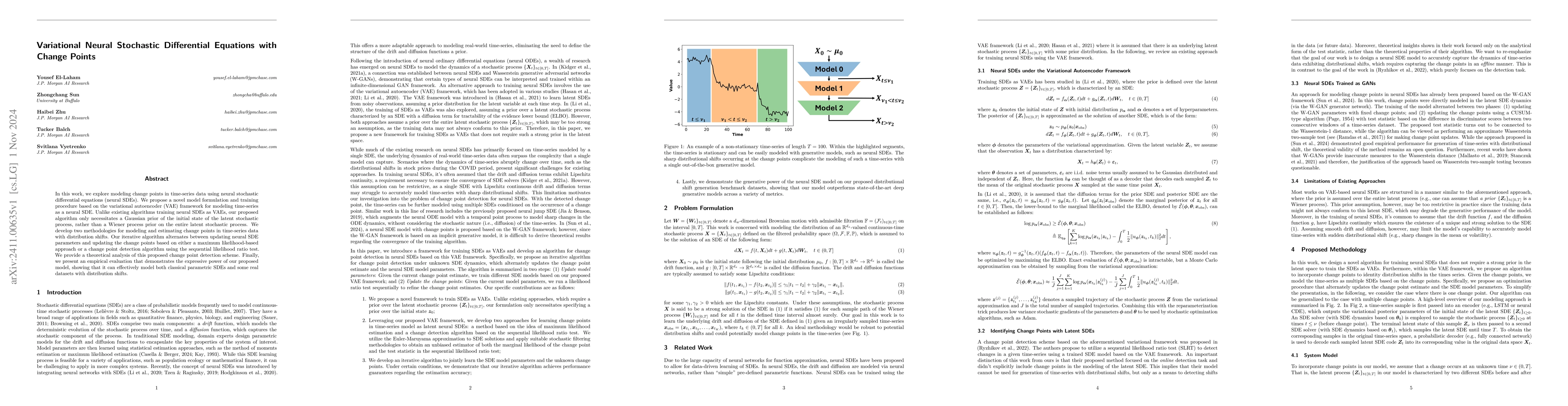

In this work, we explore modeling change points in time-series data using neural stochastic differential equations (neural SDEs). We propose a novel model formulation and training procedure based on t...

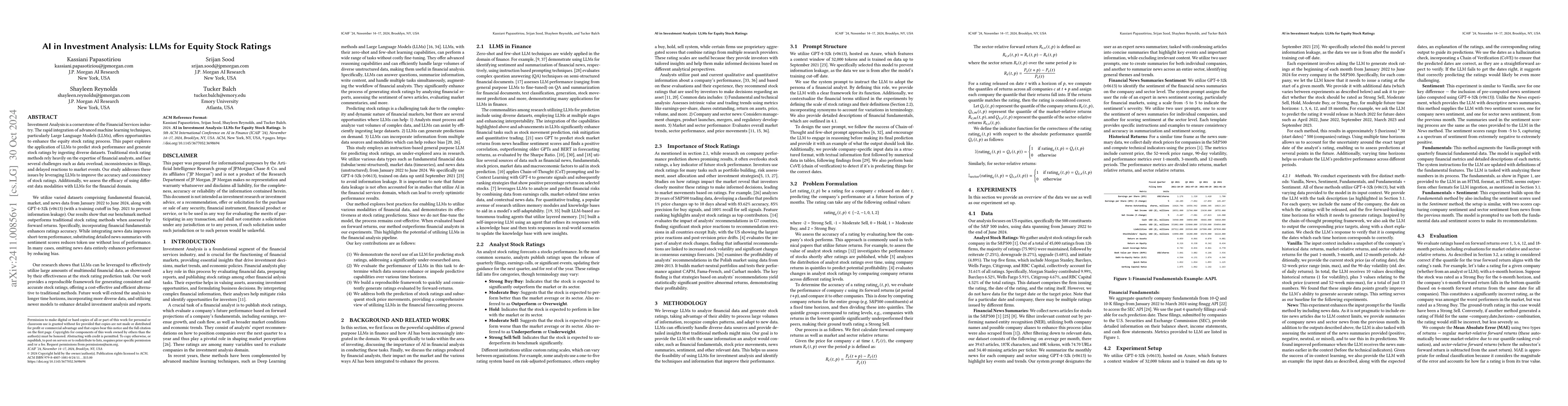

Investment Analysis is a cornerstone of the Financial Services industry. The rapid integration of advanced machine learning techniques, particularly Large Language Models (LLMs), offers opportunities ...

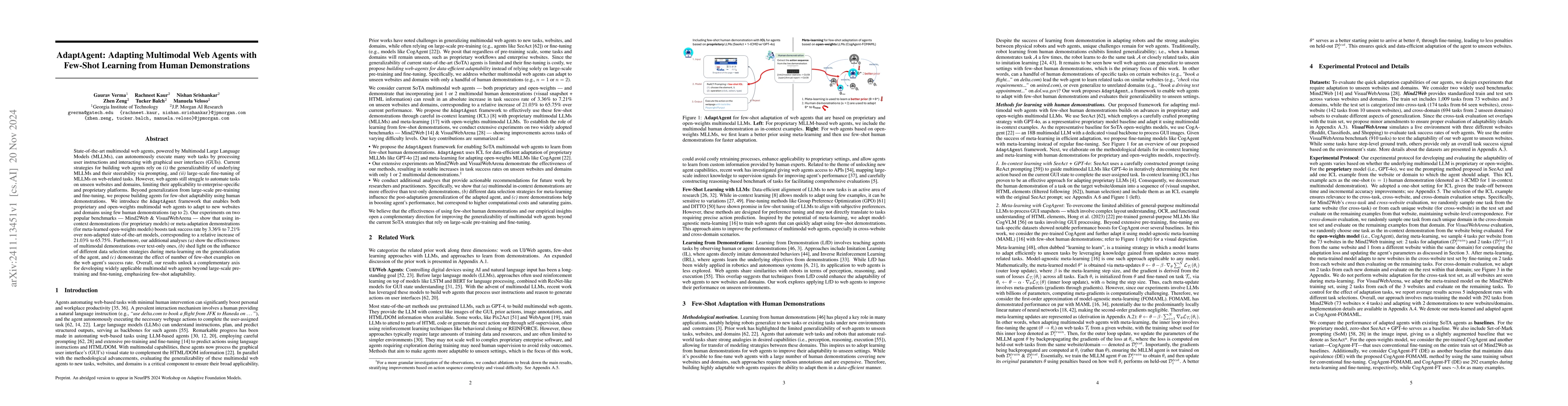

State-of-the-art multimodal web agents, powered by Multimodal Large Language Models (MLLMs), can autonomously execute many web tasks by processing user instructions and interacting with graphical user...

We present an agent-based simulator for economic systems with heterogeneous households, firms, central bank, and government agents. These agents interact to define production, consumption, and monetar...

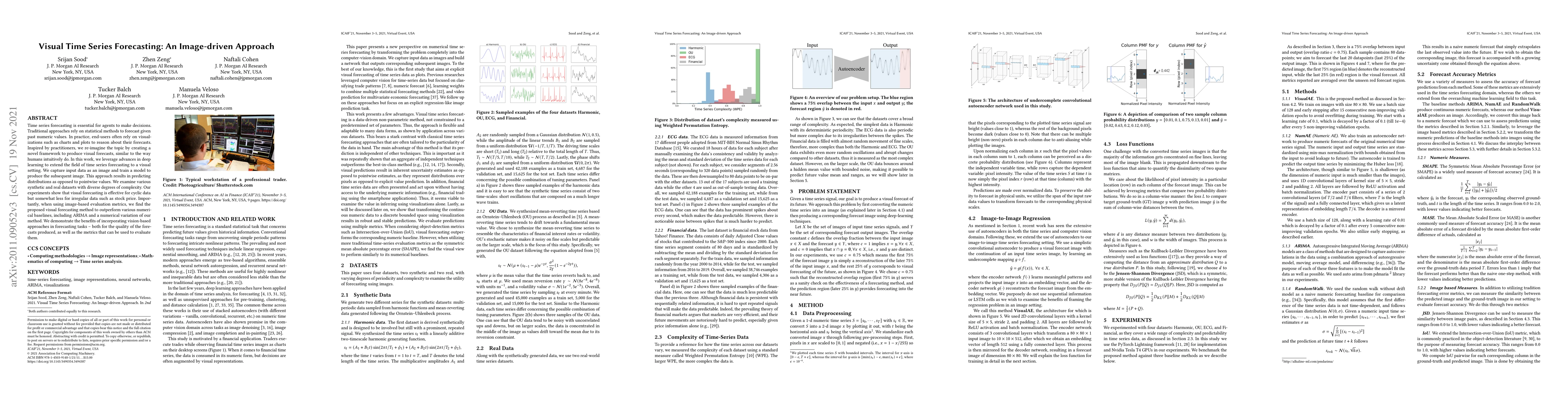

Time series forecasting is essential for agents to make decisions. Traditional approaches rely on statistical methods to forecast given past numeric values. In practice, end-users often rely on visual...

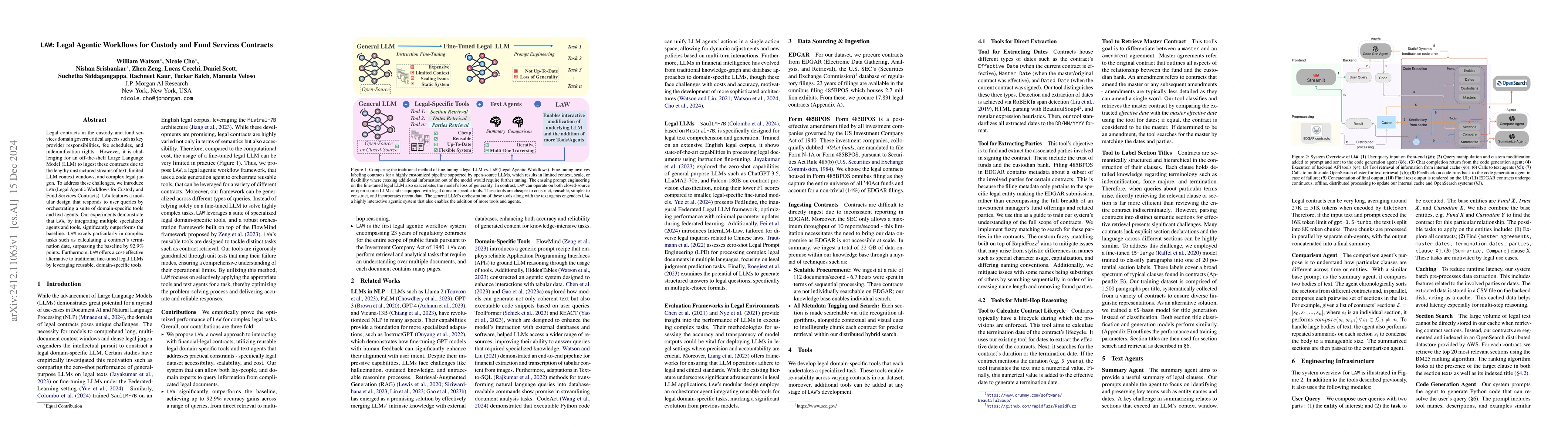

Legal contracts in the custody and fund services domain govern critical aspects such as key provider responsibilities, fee schedules, and indemnification rights. However, it is challenging for an off-...

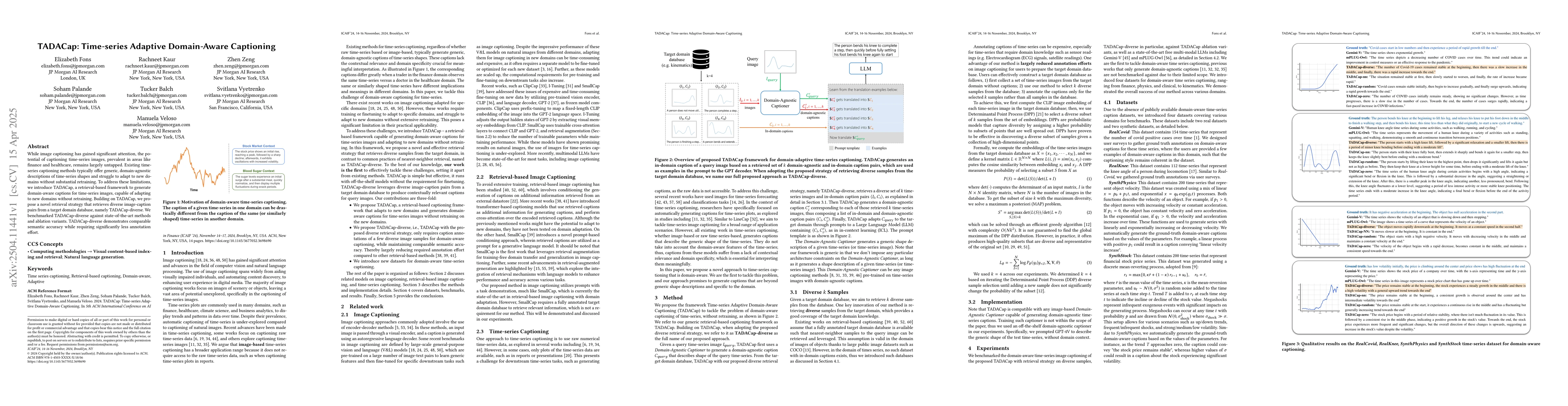

While image captioning has gained significant attention, the potential of captioning time-series images, prevalent in areas like finance and healthcare, remains largely untapped. Existing time-series ...

This paper investigates whether artificial intelligence can enhance stock clustering compared to traditional methods. We consider this in the context of the semi-strong Efficient Markets Hypothesis (E...

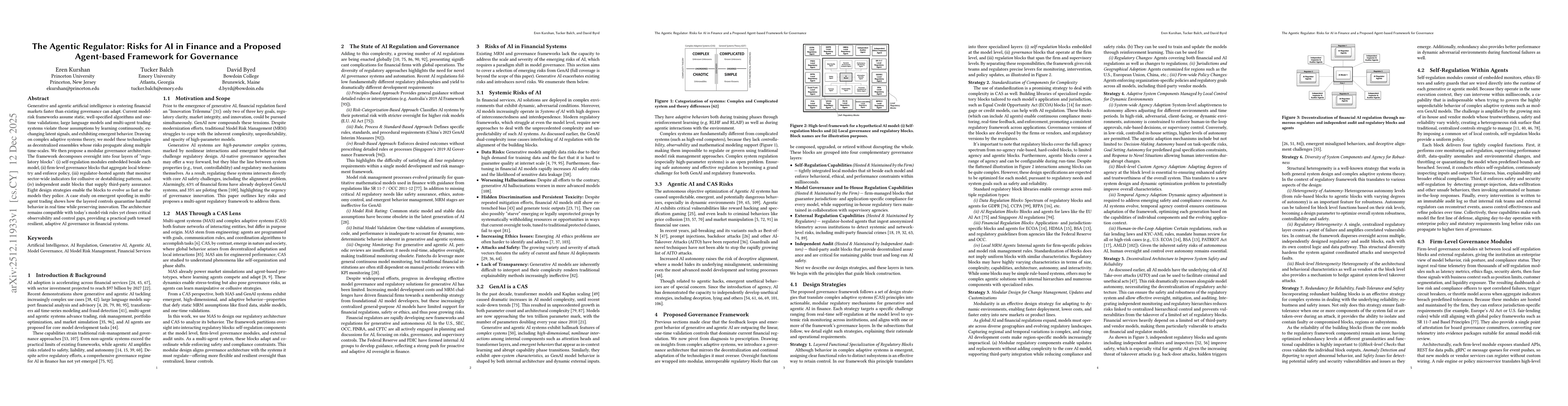

Generative and agentic artificial intelligence is entering financial markets faster than existing governance can adapt. Current model-risk frameworks assume static, well-specified algorithms and one-t...

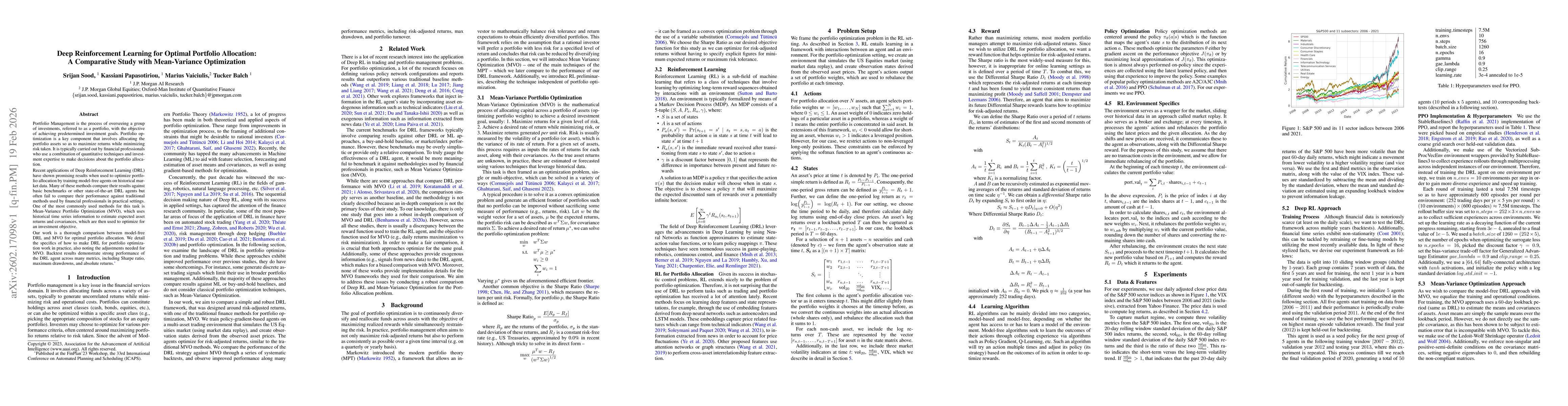

Portfolio Management is the process of overseeing a group of investments, referred to as a portfolio, with the objective of achieving predetermined investment goals. Portfolio optimization is a key co...