Academic Profile

Statistics

Similar Authors

Papers on arXiv

A multivariate quantile regression model with a factor structure is proposed to study data with many responses of interest. The factor structure is allowed to vary with the quantile levels, which ma...

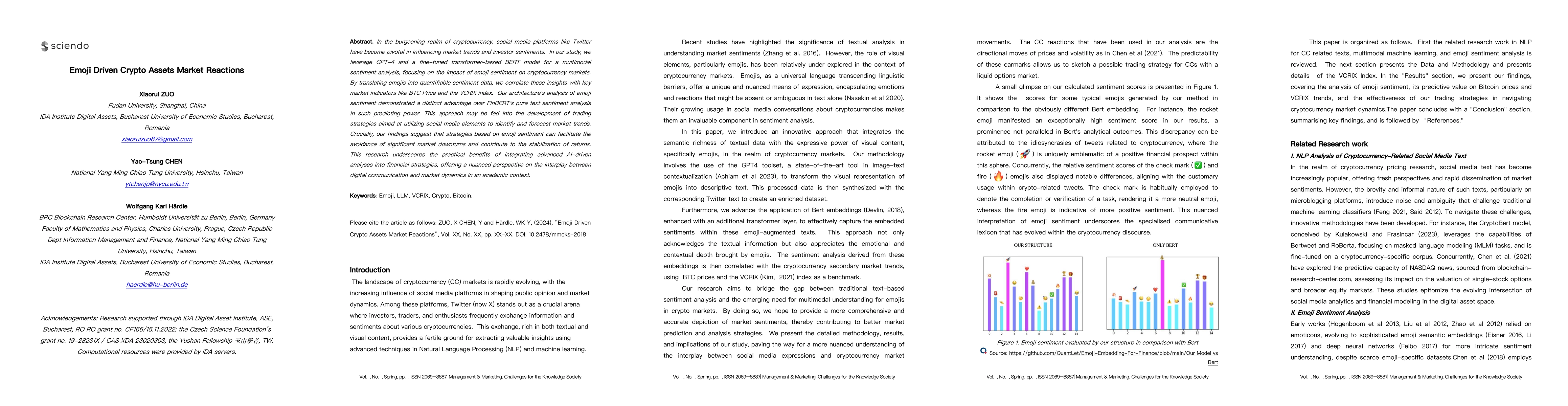

In the burgeoning realm of cryptocurrency, social media platforms like Twitter have become pivotal in influencing market trends and investor sentiments. In our study, we leverage GPT-4 and a fine-tu...

This paper explores the application of Machine Learning (ML) and Natural Language Processing (NLP) techniques in cryptocurrency price forecasting, specifically Bitcoin (BTC) and Ethereum (ETH). Focu...

Technology adoption research aims to determine the reasons why and how individuals, corporations, and industries start using new technology. Furthermore, technology adoption itself is decomposed int...

Markowitz mean-variance portfolios with sample mean and covariance as input parameters feature numerous issues in practice. They perform poorly out of sample due to estimation error, they experience...

This paper fills the limited statistical understanding of Shapley values as a variable importance measure from a nonparametric (or smoothing) perspective. We introduce population-level \textit{Shapl...

Living in the Information Age, the power of data and correct statistical analysis has never been more prevalent. Academics and practitioners require nowadays an accurate application of quantitative ...

There has been intensive research regarding machine learning models for predicting bankruptcy in recent years. However, the lack of interpretability limits their growth and practical implementation....

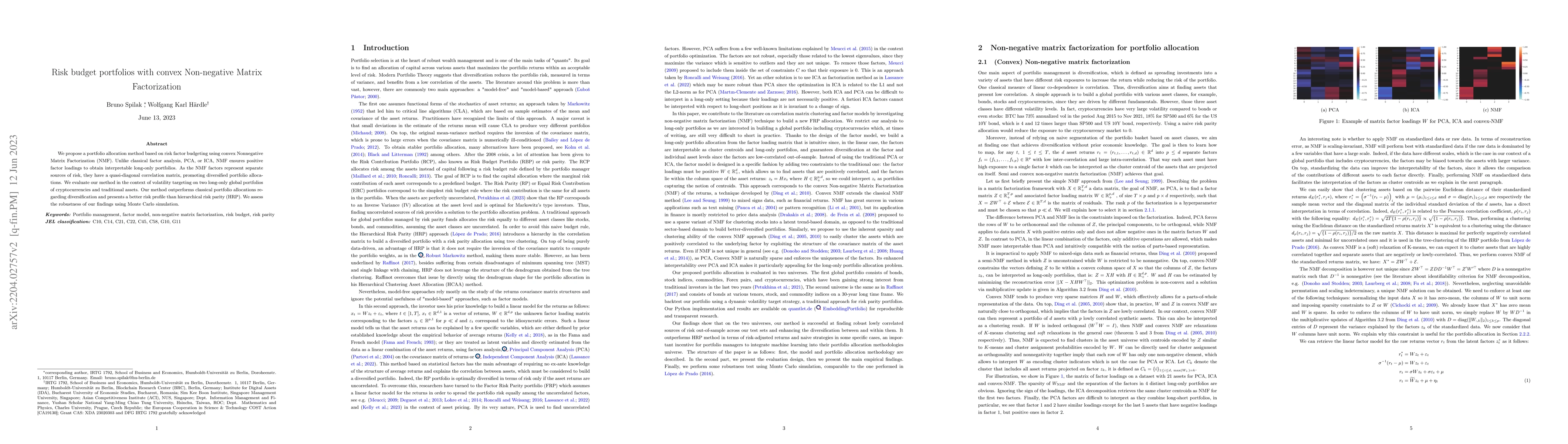

We propose a portfolio allocation method based on risk factor budgeting using convex Nonnegative Matrix Factorization (NMF). Unlike classical factor analysis, PCA, or ICA, NMF ensures positive facto...

The cryptocurrency market is volatile, non-stationary and non-continuous. Together with liquid derivatives markets, this poses a unique opportunity to study risk management, especially the hedging o...

While attention is a predictor for digital asset prices, and jumps in Bitcoin prices are well-known, we know little about its alternatives. Studying high frequency crypto data gives us the unique po...

Cryptocurrencies return cross-predictability and technological similarity yield information on risk propagation and market segmentation. To investigate these effects, we build a time-varying network...

Excessive house price growth was at the heart of the financial crisis in 2007/08. Since then, many countries have added cooling measures to their regulatory frameworks. It has been found that these ...

We uncover networks from news articles to study cross-sectional stock returns. By analyzing a huge dataset of more than 1 million news articles collected from the internet, we construct time-varying...

We model the dynamics of the cryptocurrency (CC) asset class via a stochastic volatility with correlated jumps (SVCJ) model with rolling-window parameter estimates. By analyzing the time-series of p...

$K$-means clustering is one of the most widely-used partitioning algorithm in cluster analysis due to its simplicity and computational efficiency. However, $K$-means does not provide an appropriate ...

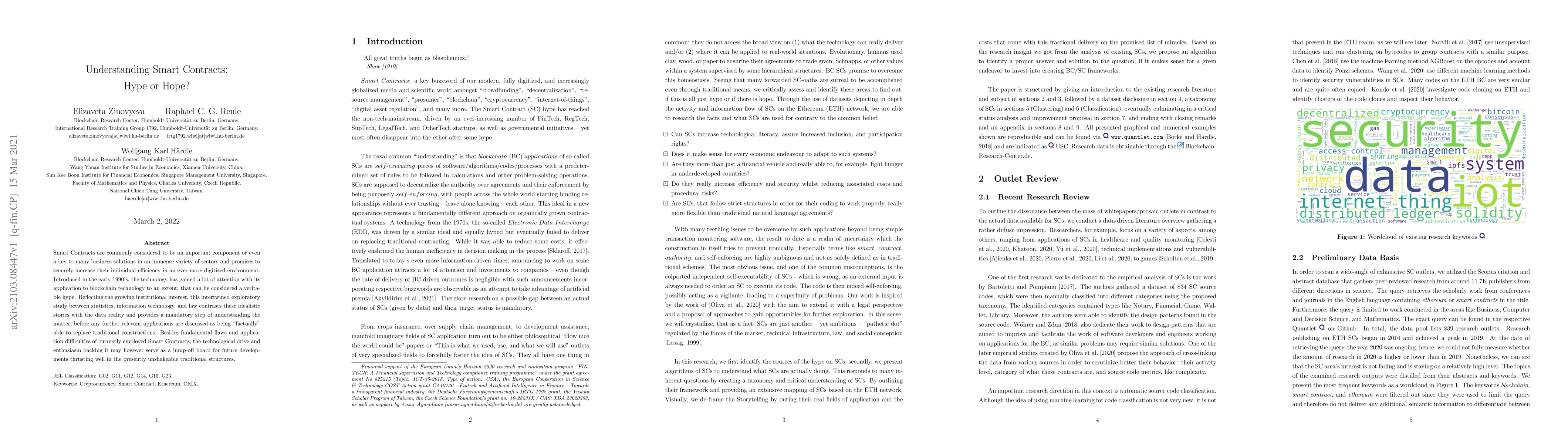

Smart Contracts are commonly considered to be an important component or even a key to many business solutions in an immense variety of sectors and promises to securely increase their individual effi...

The fast-growing Emerging Market (EM) economies and their improved transparency and liquidity have attracted international investors. However, the external price shocks can result in a higher level ...

The integration of social media characteristics into an econometric framework requires modeling a high dimensional dynamic network with dimensions of parameter typically much larger than the number ...

Driven by increased complexity of dynamical systems, the solution of system of differential equations through numerical simulation in optimization problems has become computationally expensive. This...

Strategic planning in a corporate environment is often based on experience and intuition, although internal data is usually available and can be a valuable source of information. Predicting merger &...

We investigate the relationship between underlying blockchain mechanism of cryptocurrencies and its distributional characteristics. In addition to price, we emphasise on using actual block size and ...

Penalized spline smoothing of time series and its asymptotic properties are studied. A data-driven algorithm for selecting the smoothing parameter is developed. The proposal is applied to define a s...

Tail risk protection is in the focus of the financial industry and requires solid mathematical and statistical tools, especially when a trading strategy is derived. Recent hype driven by machine lea...

AI artificial intelligence brings about new quantitative techniques to assess the state of an economy. Here we describe a new measure for systemic risk: the Financial Risk Meter (FRM). This measure ...

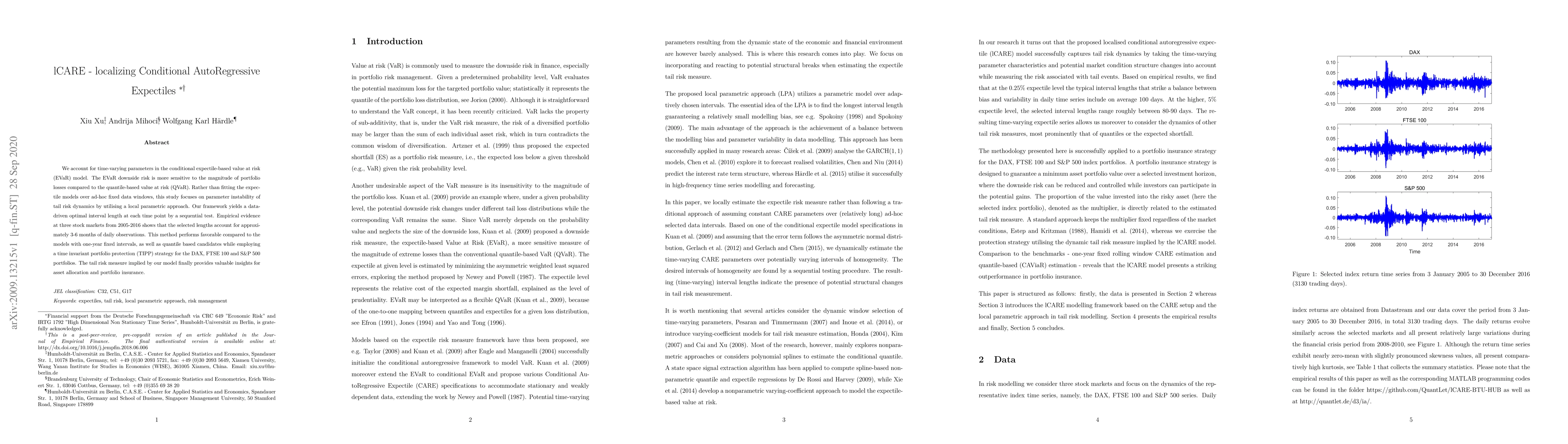

We account for time-varying parameters in the conditional expectile-based value at risk (EVaR) model. The EVaR downside risk is more sensitive to the magnitude of portfolio losses compared to the qu...

In order to price contingent claims one needs to first understand the dynamics of these indices. Here we provide a first econometric analysis of the CRIX family within a time-series framework. The k...

Cryptocurrencies' values often respond aggressively to major policy changes, but none of the existing indices informs on the market risks associated with regulatory changes. In this paper, we quanti...

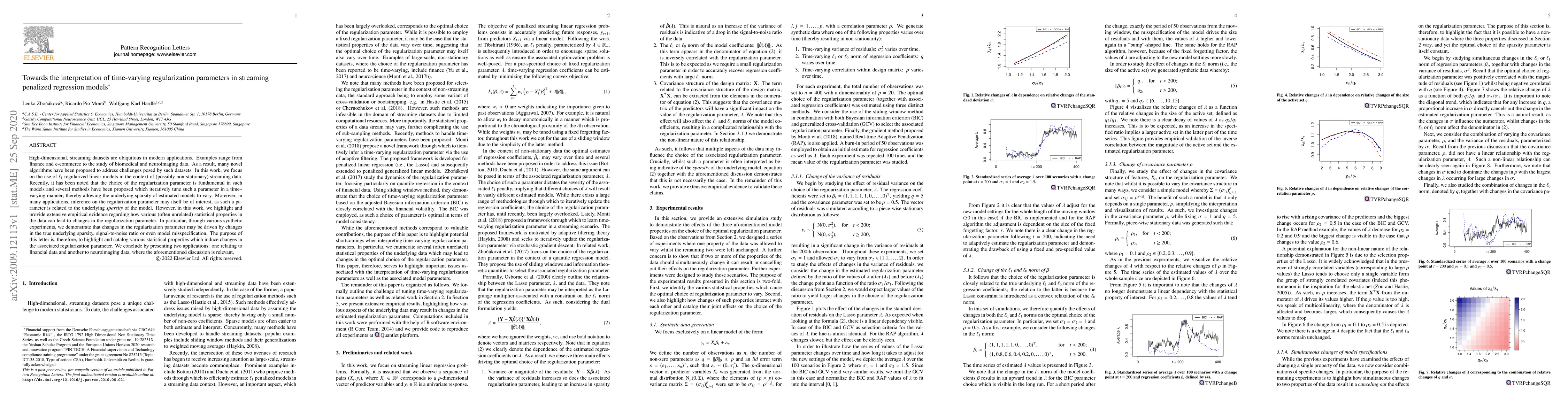

High-dimensional, streaming datasets are ubiquitous in modern applications. Examples range from finance and e-commerce to the study of biomedical and neuroimaging data. As a result, many novel algor...

A standard quantitative method to access credit risk employs a factor model based on joint multivariate normal distribution properties. By extending a one-factor Gaussian copula model to make a more...

Monthly disaggregated US data from 1978 to 2016 reveals that exposure to news on inflation and monetary policy helps to explain inflation expectations. This remains true when controlling for househo...

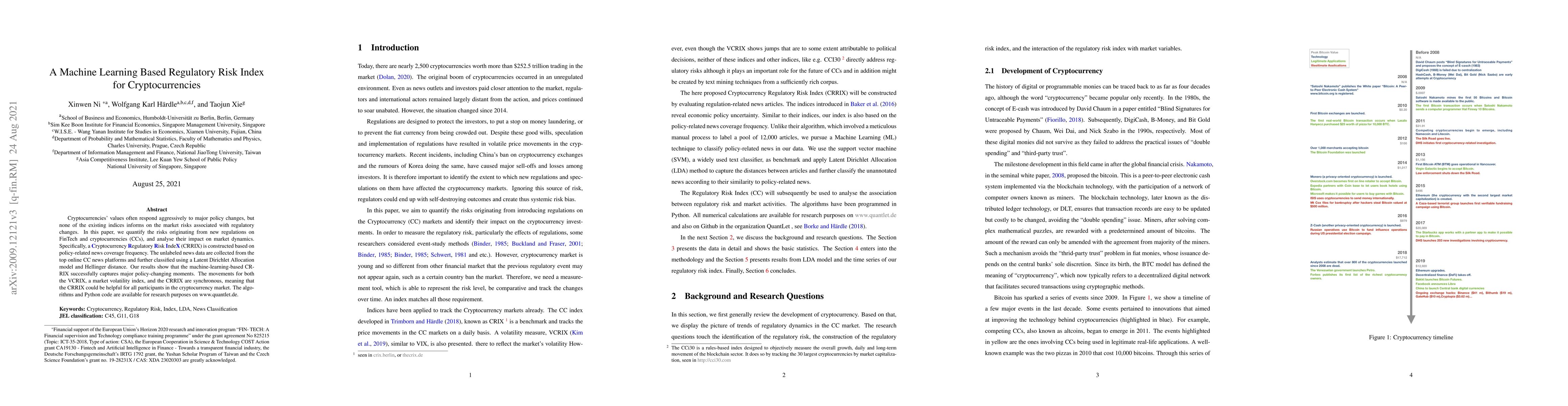

Cryptocurrencies, especially Bitcoin (BTC), which comprise a new digital asset class, have drawn extraordinary worldwide attention. The characteristics of the cryptocurrency/BTC include a high level...

The gargantuan plethora of opinions, facts and tweets on financial business offers the opportunity to test and analyze the influence of such text sources on future directions of stocks. It also crea...

The cryptocurrency market is unique on many levels: Very volatile, frequently changing market structure, emerging and vanishing of cryptocurrencies on a daily level. Following its development became...

Equity basket correlation can be estimated both using the physical measure from stock prices, and also using the risk neutral measure from option prices. The difference between the two estimates mot...

In this paper we propose a regularization approach for network modeling of German power derivative market. To deal with the large portfolio, we combine high-dimensional variable selection techniques...

In this paper, we study the statistical properties of the moneyness scaling transformation by Leung and Sircar (2015). This transformation adjusts the moneyness coordinate of the implied volatility ...

New Public Management helps universities and research institutions to perform in a highly competitive research environment. Evaluating publicly financed research improves transparency, helps in refl...

Appropriate risk management is crucial to ensure the competitiveness of financial institutions and the stability of the economy. One widely used financial risk measure is Value-at-Risk (VaR). VaR es...

The Generalized Additive Model (GAM) is a powerful tool and has been well studied. This model class helps to identify additive regression structure. Via available test procedures one may identify th...

In this study, we develop nonparametric analysis of deviance tools for generalized partially linear models based on local polynomial fitting. Assuming a canonical link, we propose expressions for bo...

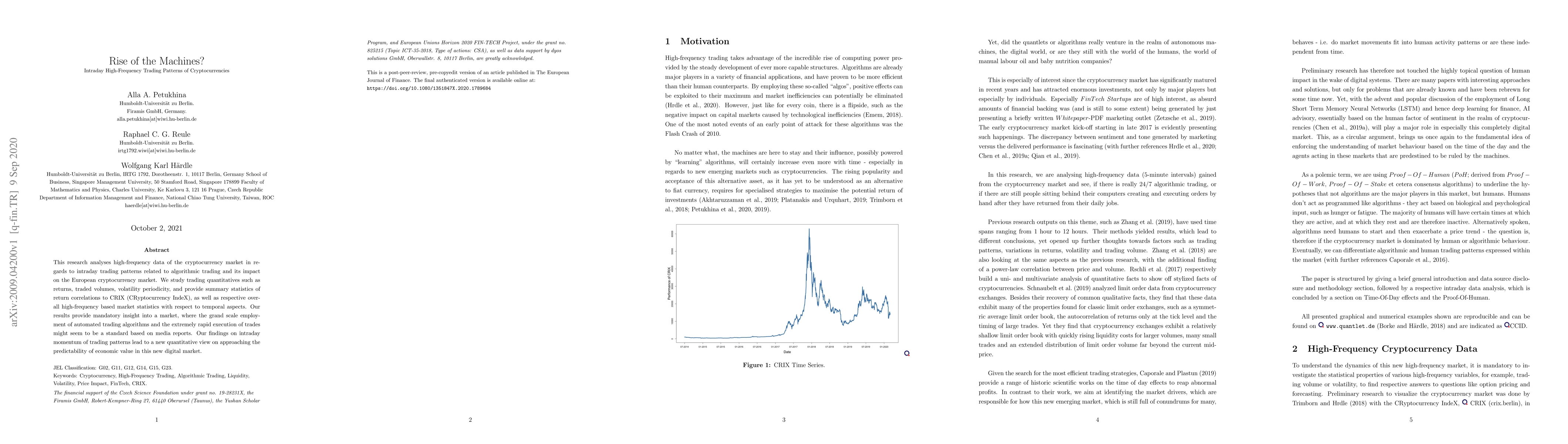

This research analyses high-frequency data of the cryptocurrency market in regards to intraday trading patterns related to algorithmic trading and its impact on the European cryptocurrency market. W...

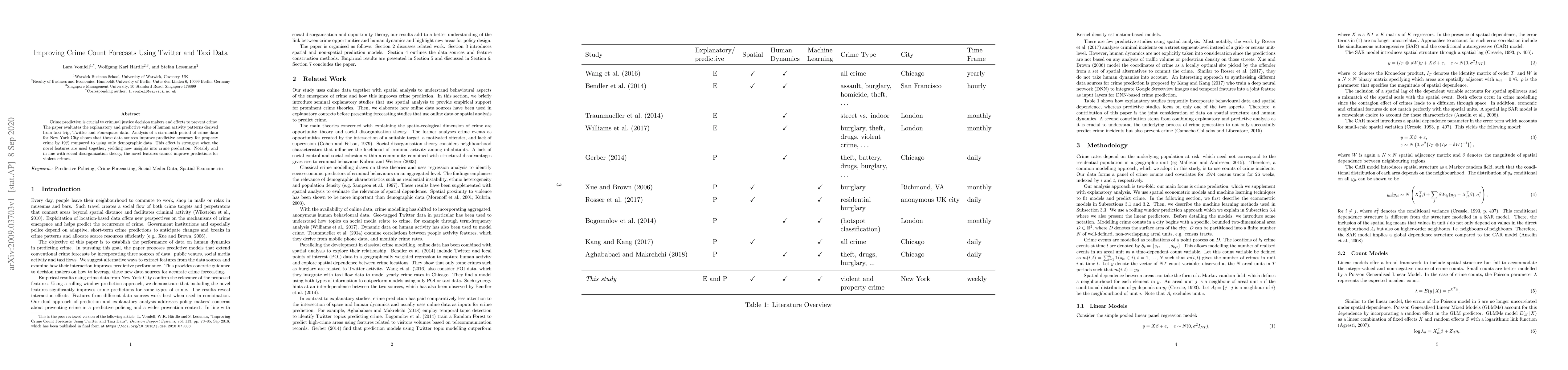

Crime prediction is crucial to criminal justice decision makers and efforts to prevent crime. The paper evaluates the explanatory and predictive value of human activity patterns derived from taxi tr...

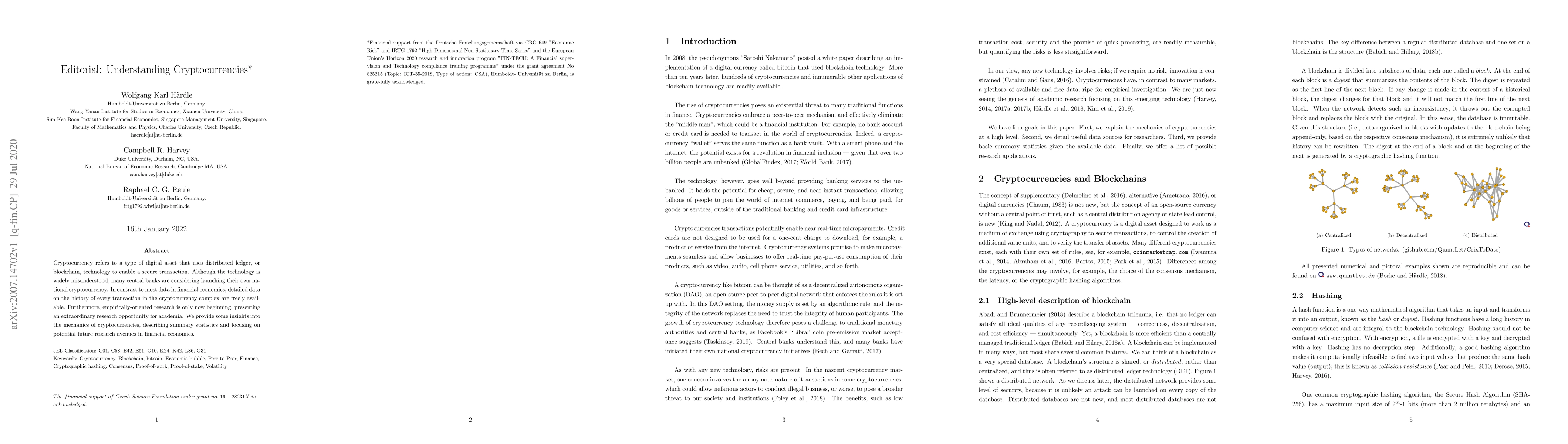

Cryptocurrency refers to a type of digital asset that uses distributed ledger, or blockchain, technology to enable a secure transaction. Although the technology is widely misunderstood, many central...

Cryptocurrency, the most controversial and simultaneously the most interesting asset, has attracted many investors and speculators in recent years. The visibly significant market capitalization of c...